The Economics of Agentic Commerce: Revenue Models, Margins, and Merchant Impact

The agentic commerce landscape of 2026 represents a fundamental shift in how transactions occur, who captures value, and where margins are distributed. Unlike traditional e-commerce where merchants maintain direct customer relationships, agentic commerce introduces autonomous agents as intermediaries—software entities that discover products, negotiate terms, execute purchases, and manage post-transaction relationships on behalf of consumers. This architectural change creates new revenue streams while simultaneously compressing traditional merchant margins.

Understanding Agentic Payments Architecture

Agentic payments differ fundamentally from conventional payment processing. Rather than a consumer initiating a transaction through a merchant’s website or app, autonomous agents connected to the Universal Commerce Protocol (UCP) identify optimal purchase opportunities across distributed merchant networks. These agents leverage real-time pricing data, inventory visibility, and merchant APIs to execute transactions that maximize consumer utility—whether through price optimization, convenience, or product discovery.

Related articles: UCP Shipping Carrier Selection & Rate Optimization • UCP Security Best Practices for AI-Driven Commerce

The economic model hinges on several key participants: agents (owned by consumers or aggregators), merchants (product/service providers), payment processors, and protocol infrastructure providers. Each participant captures value differently, creating a more fragmented but potentially more efficient commerce ecosystem.

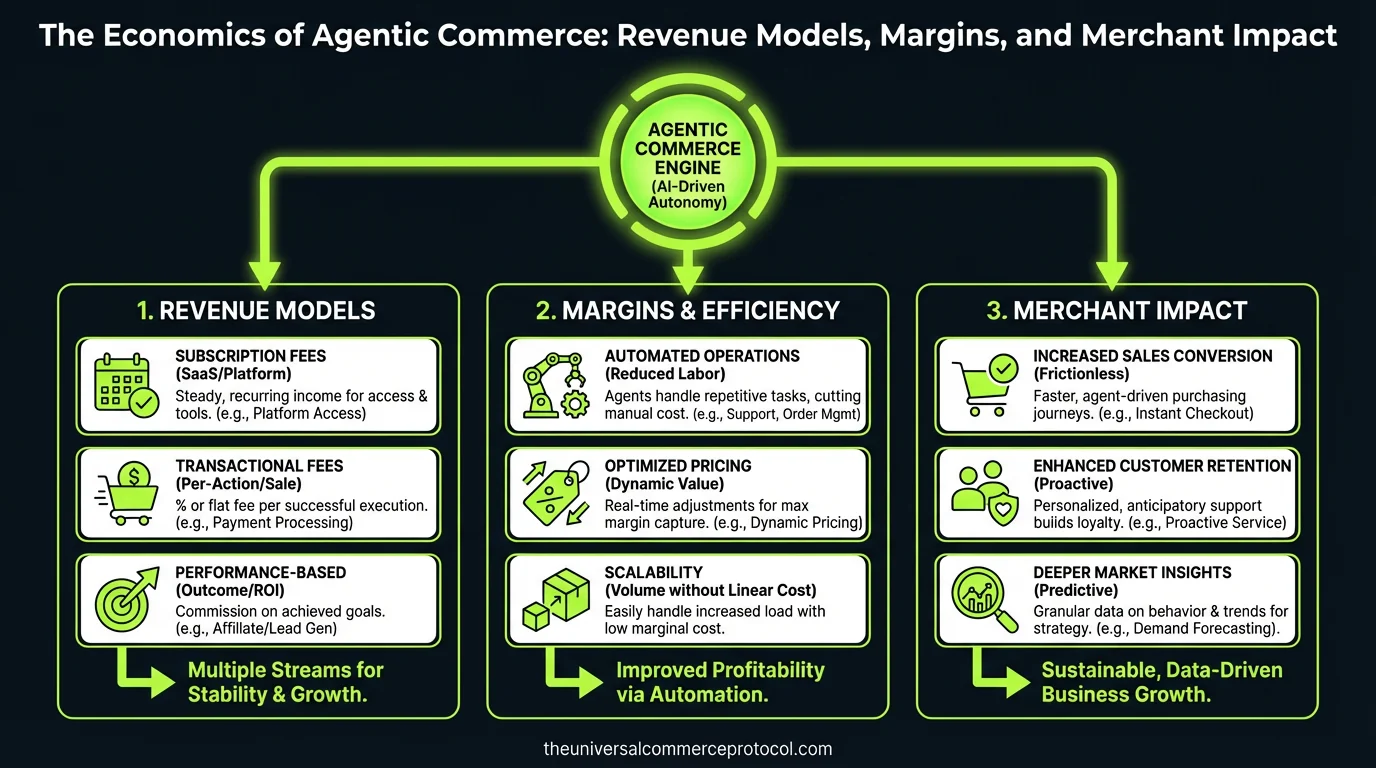

Revenue Models Emerging in 2026

The primary revenue models for agentic commerce platforms include:

- Transaction-based fees: Platforms like Stripe and Square have adapted their payment processing to accommodate agentic transactions, typically charging 2.2% + $0.30 per transaction. However, agentic commerce’s higher transaction volume and lower average order value (due to agent-driven micro-purchases) compress these margins significantly.

- Agent licensing: Companies like Anthropic and OpenAI monetize agent capabilities through API usage. As of Q2 2026, Claude’s agentic API pricing stands at $0.003 per 1K input tokens and $0.015 per 1K output tokens—substantially lower than previous models but compensated by volume.

- Protocol infrastructure fees: UCP-compliant platforms charge merchants for API access, data synchronization, and agent integration. These typically range from $500-$5,000 monthly for mid-market retailers.

- Data monetization: Aggregated consumer preference data, purchasing patterns, and price sensitivity insights generated through agentic transactions represent a new revenue stream. Privacy-compliant data licensing generates 8-12% additional revenue for major platforms.

- Merchant premium services: Merchants pay for priority visibility within agent decision-making algorithms, similar to sponsored listings but more sophisticated. Amazon’s recent “Agent Preferred” program charges 3-5% of transaction value.

Margin Compression for Traditional Merchants

Traditional e-commerce merchants face unprecedented margin pressure in the agentic commerce environment. Historical gross margins in online retail averaged 35-45%, with net margins typically 5-15% after fulfillment, marketing, and operational costs. Agentic commerce disrupts this model through several mechanisms:

Price transparency and algorithmic competition: Agents continuously compare prices across merchant networks in real-time. A merchant selling electronics at a 2% premium to competitors loses agent-directed traffic immediately. This has compressed average margins in competitive categories from 25% to 12-18% by mid-2026. Electronics retailers like Best Buy and Micro Center have absorbed the steepest margin compression, while niche and brand-differentiated merchants maintain stronger positions.

Increased transaction costs: Each agentic transaction requires API calls, data verification, and protocol compliance checks. These infrastructure costs add 0.8-1.5% to transaction processing expenses. When combined with traditional payment processing fees, total transaction costs now reach 3.5-4.5% for agentic commerce versus 2.5-3% for traditional e-commerce.

Fulfillment complexity: Agents optimize for consumer value, which frequently means directing orders to merchants offering faster shipping or lower fulfillment costs. This creates a “fulfillment arms race” where merchants must invest in faster logistics to remain competitive. Shopify merchants report fulfillment cost increases of 12-18% since widespread agent adoption began in late 2025.

Platform Economics and Value Capture

Payment platforms and commerce infrastructure providers have benefited substantially from agentic commerce’s growth. Stripe processed $47 billion in agentic commerce transactions in 2026 (representing 18% of total processed volume), with transaction fees generating $1.03 billion in revenue. However, the economics differ from traditional payments:

Agentic transactions average $23 in order value compared to $67 for traditional e-commerce—a 66% reduction. This necessitates higher transaction volumes to maintain revenue. Stripe compensated through volume growth (340% increase in agentic transaction count year-over-year) and tiered pricing models. Enterprise merchants receive 1.8% + $0.10 pricing, while small merchants pay 2.9% + $0.30.

PayPal’s agentic commerce initiative, launched Q3 2025, targets a different margin model. Rather than competing on transaction fees, PayPal charges merchants 1.5% for agentic payment processing while capturing value through merchant financing products. By offering working capital advances to merchants experiencing cash flow strain from margin compression, PayPal generates 18-24% annualized returns on merchant lending—substantially higher than traditional payment processing margins.

Agent Aggregator Economics

A new category of intermediaries—agent aggregators—has emerged to capture value from agentic commerce. Companies like Perplexity Shopping (powered by Perplexity’s agent infrastructure) and specialized commerce agents operate as consumer agents, directing purchase decisions to merchants offering optimal terms. These aggregators typically capture 1-3% of transaction value through merchant rebates or direct commission arrangements.

The economics favor scale dramatically. An agent aggregator with 5 million active users directing $50 average monthly spend generates $3 billion in annual transaction volume. At 1.5% capture rate, this produces $45 million annual revenue. However, customer acquisition costs remain substantial—$12-$18 per user through advertising—requiring 18-24 months for payback.

Merchant Category Performance

Agentic commerce impacts different merchant categories asymmetrically:

- Commoditized goods (electronics, home goods): Margin compression of 40-50%. Merchants compete primarily on price and fulfillment speed. Amazon, Walmart, and specialized retailers with cost advantages dominate.

- Brand-differentiated products (luxury, fashion, beauty): Margin compression of 15-25%. Brand loyalty and product differentiation provide protection against pure price competition. Brands like Nike, Yeti, and Dyson maintain 28-35% gross margins despite agent competition.

- Services and subscriptions: Margin impact minimal (5-10% compression). Agent optimization in services focuses on convenience and feature matching rather than price. SaaS providers and subscription services report stable margins.

- Long-tail and specialty products: Margin expansion in certain segments. Agents excel at discovering niche products matching specific consumer preferences. Etsy sellers report 8-12% margin improvement as agents direct highly-qualified buyers to specialty listings.

Strategic Responses and Margin Preservation

Merchants implementing successful strategies to preserve margins include:

- Direct agent relationships: Merchants like Costco and Target negotiate direct integrations with major agents, offering preferred pricing and inventory visibility in exchange for priority placement. This creates a “walled garden” economics model that preserves 5-8% margin premium.

- Vertical integration: Merchants controlling fulfillment infrastructure (Amazon, Walmart, Best Buy) maintain 3-5% margin advantage over pure-play online retailers through lower fulfillment costs.

- Subscription and loyalty programs: Merchants offering subscription tiers or loyalty programs to agents (e.g., “Agent Prime” benefits) create switching costs that protect margins by 2-4%.

- Private label and exclusive products: Brands developing exclusive SKUs unavailable through competitors preserve 15-20% margin premiums since agents cannot arbitrage pricing on unique products.

Looking Forward: 2026 and Beyond

The agentic payments ecosystem in 2026 remains in active consolidation. Transaction volumes are growing 280-320% annually, while merchant margins compress 2-3% quarterly in competitive categories. Platform economics favor aggregators and infrastructure providers, while traditional merchants face structural margin pressure requiring strategic adaptation.

The long-term equilibrium remains unclear. If agentic commerce captures 40-50% of e-commerce volume (projected by 2028), the resulting margin compression could trigger significant merchant consolidation, with only cost-advantaged and differentiated players surviving profitably. Alternatively, merchant adaptation through direct agent relationships and exclusive products could stabilize margins at 20-25% gross levels—still compressed from historical 35-40% but sustainable.

FAQ

How do agentic payments differ from traditional payment processing in terms of cost structure?

Agentic payments involve additional infrastructure costs (0.8-1.5%) beyond traditional payment processing fees due to API calls, protocol compliance, and data verification requirements. However, higher transaction volumes and competitive fee pressure from Stripe, PayPal, and emerging platforms have compressed overall transaction costs. The key difference is that merchants face variable costs beyond payment processing—fulfillment optimization, agent visibility fees, and margin compression from price transparency.

What revenue models are most sustainable for agentic commerce platforms in 2026?

Transaction-based fees remain the largest revenue source but face compression due to volume competition. More sustainable models include: (1) merchant premium services and agent visibility ranking (3-5% of transaction value), (2) consumer subscription tiers for enhanced agent capabilities ($9.99-$29.99 monthly), and (3) merchant financing and working capital products (18-24% annualized returns). Platforms combining multiple revenue streams report better margin stability than those relying solely on transaction fees.

Which merchant categories are most impacted by agentic commerce margin compression?

Commoditized goods categories (electronics, home goods, basic apparel) experience 40-50% margin compression due to intense price competition among agents. Brand-differentiated categories (luxury, premium fashion, specialized tools) compress 15-25% as brand loyalty provides pricing power. Services and subscriptions see minimal impact (5-10%), while long-tail specialty products may see margin expansion as agents efficiently match niche products to qualified buyers.

What strategies enable merchants to preserve margins in agentic commerce environments?

Successful margin preservation strategies include: (1) direct agent relationship agreements offering preferred pricing and inventory visibility, (2) vertical integration of fulfillment to reduce costs below competitors, (3) subscription or loyalty programs creating switching costs, and (4) exclusive private label products that agents cannot arbitrage. Merchants combining 2-3 of these strategies maintain gross margins within 5-10% of pre-agentic levels, while those relying solely on price competition see 40%+ margin compression.

Frequently Asked Questions

What is the Universal Commerce Protocol (UCP)?

The Universal Commerce Protocol (UCP) is an open standard developed to enable AI agents to autonomously conduct commerce transactions across any platform.

How does UCP enable agentic commerce?

UCP provides standardized APIs and protocols so AI agents can discover products, negotiate terms, and complete purchases without human intervention, working across any compatible commerce platform.

Why should businesses implement UCP?

UCP adoption reduces integration costs, opens revenue channels to AI-driven buyers, and future-proofs commerce infrastructure as agentic purchasing becomes mainstream.

Leave a Reply