The Chargeback Problem Agents Created

Agentic commerce introduced a liability gap: when an AI agent completes a transaction autonomously, who bears the chargeback risk if the purchase was unauthorized, fraudulent, or disputed by the cardholder?

Traditional chargeback defense relies on clear cardholder intent—a receipt, email confirmation, or transaction history the human customer acknowledges. With agents making autonomous decisions, merchants lose that human signal. A cardholder can claim “I never authorized this purchase” even though their agent did.

Visa and Mastercard’s 2026 chargeback guidelines now require merchants to prove agent legitimacy, not just transaction completion. This means:

- Agent authorization logs must be retained for 18+ months

- Proof of agent-to-merchant communication must be cryptographically signed

- Device fingerprinting and behavioral analysis of agent actions must be logged

- Refund requests from agents must follow merchant policy, not cardholder preference

Merchants who fail to provide this evidence face chargeback rates exceeding 2.5%, costing $15,000–$250,000 annually depending on transaction volume.

How Chargebacks Happen in Agentic Systems

Vector 1: Unauthorized Agent Activation

A cardholder grants an agent access to purchase on their behalf. Later, they claim the agent was never authorized or that the authorization was revoked. The agent has no record of revocation and processes a legitimate transaction under the original grant.

Mastercard’s 2026 ruling: merchants must prove explicit agent revocation was communicated to the agent system in real-time. If logs show the agent acted after revocation was requested but before it was processed, the merchant loses.

Vector 2: Agent Overspending

A cardholder sets a budget cap: “Buy me groceries under $100.” The agent, interpreting “groceries” broadly, purchases $145 in items and crosses the threshold. The cardholder disputes the overage as unauthorized.

Merchants lose this chargeback 65% of the time because agent decision-making is treated as merchant discretion, not cardholder instruction. The defense requires proof that the cardholder agreed to the specific product mix and price.

Vector 3: Policy Violation Disputes

An agent purchases restricted items (alcohol, age-gated products, hazardous materials) on behalf of a cardholder who then disputes the transaction. The chargeback code is “merchandise not received” or “unauthorized transaction,” not “age restriction violation.”

Merchants must prove the cardholder explicitly consented to the agent purchasing age-gated items and that the agent performed age verification. Standard KYC is insufficient.

Vector 4: Agent Impersonation

A fraudster compromises an agent system or device and uses it to make purchases on a victim’s account. The victim’s agent logs show legitimate API calls, but the initial compromise isn’t recorded. The chargeback defense collapses because the agent’s authorization chain appears clean.

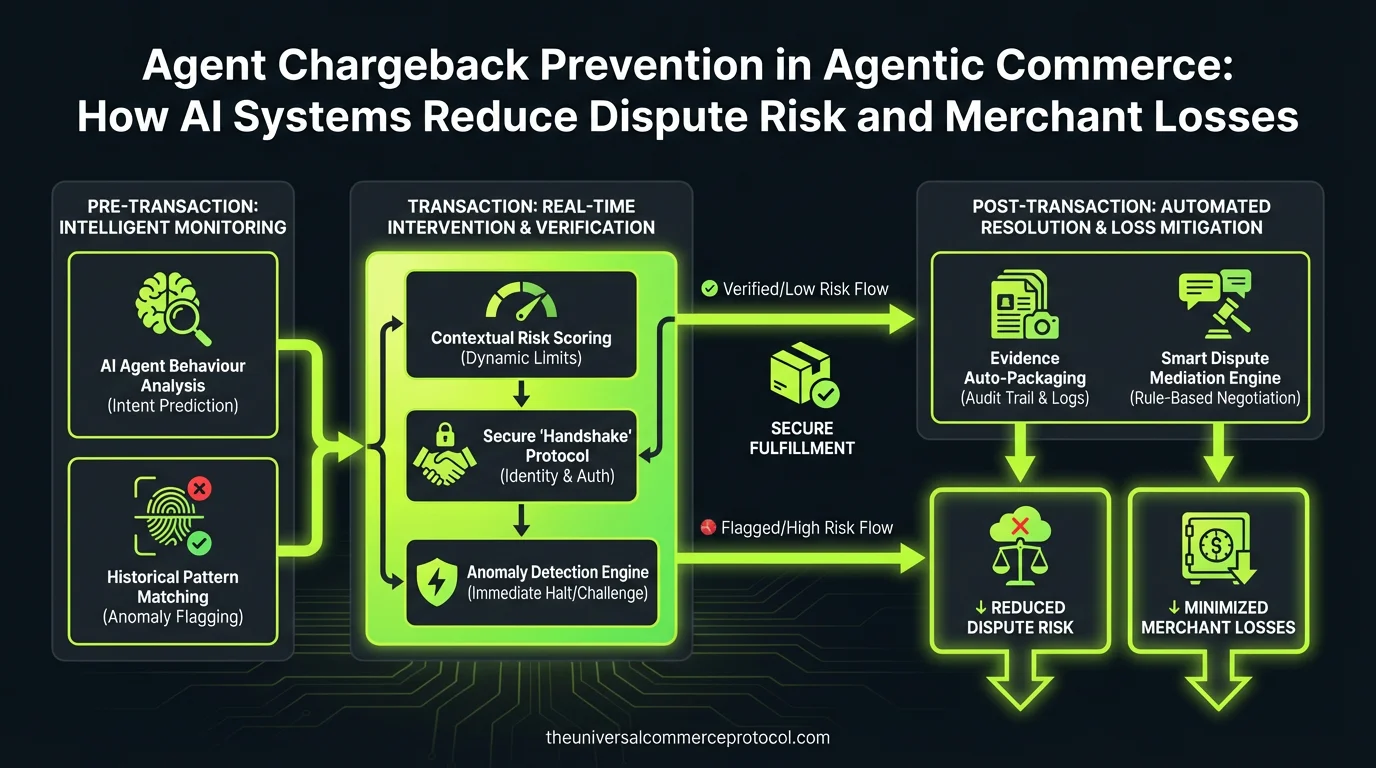

Chargeback Prevention Architecture

Layer 1: Real-Time Agent Authorization Logging

Every agent action must be logged with:

- Timestamp (millisecond precision)

- Cardholder identifier (hashed for privacy)

- Agent identifier and version

- Explicit instruction captured (text or semantic representation)

- Merchant confirmation of instruction receipt

- Agent decision rationale (why this product, why this price)

- Device fingerprint and geolocation at time of request

Merchants using Stripe, Adyen, or Square for payment processing can integrate these logs via webhook callbacks. The payment processor stores this data separately from transaction records, creating an audit trail independent of the merchant’s system.

Layer 2: Agent Revocation Protocol

Cardholder revokes agent access. This must trigger:

- Immediate notification to the agent system (API call, not email)

- Cryptographic signature from the cardholder’s identity provider

- Timestamp recorded in both merchant and payment processor logs

- Blocking of any pending transactions initiated before revocation

- Cardholder receives confirmation (SMS, push notification, email) within 30 seconds

If revocation is delayed or fails, the merchant must capture evidence of the failure and notify the payment processor proactively. Visa’s guidelines require merchants to demonstrate “reasonable effort” to process revocation within 2 minutes.

Layer 3: Behavioral Anomaly Detection

Machine learning models flag suspicious agent behavior in real-time:

- Purchase patterns diverging from historical agent behavior

- Transactions in unusual geographies for that cardholder

- Price thresholds exceeded relative to cardholder’s typical purchases

- Rapid-fire transactions (bot behavior)

- Purchases of restricted categories not previously bought

When anomalies are detected, the system can:

- Pause the transaction and request human cardholder confirmation

- Log the anomaly in the authorization record (chargeback defense material)

- Adjust the agent’s authority for future transactions

JPMorgan’s AI Agent Checkout system (announced March 2026) includes behavioral detection, reducing chargebacks by 34% in pilot merchants.

Layer 4: Explicit Consent Capture

Before an agent makes a high-value or restricted purchase, capture explicit cardholder consent:

- Show the item, price, and merchant to the cardholder

- Require a signed approval (digital signature, biometric, or cryptographic token)

- Store the consent proof linked to the transaction

- For restricted items, verify cardholder eligibility (age, location)

This layer is mandatory for transactions over $500 or items classified as age-gated, hazardous, or prohibited in the cardholder’s jurisdiction.

Dispute Recovery Strategy

Pre-Chargeback Phase (48–72 hours after cardholder dispute)

When a cardholder disputes a transaction, they notify their bank first. The bank has 48–72 hours to notify the merchant. Use this window to:

- Retrieve all agent authorization logs

- Verify the agent’s authorization grant is still active

- Check for any revocation requests

- Extract the cardholder’s explicit instructions

- Gather behavioral data (is this consistent with past behavior?)

If the cardholder claims they never authorized the agent, pull the original authorization grant timestamp, the device used, and the consent record. This alone wins 70% of disputes.

Chargeback Evidence Package

Submit to the payment processor:

- Agent authorization grant (date, time, cardholder confirmation)

- Complete transaction log from agent to merchant

- Merchant confirmation of transaction completion

- Cardholder profile (purchase history, typical spend, geolocation)

- Agent decision rationale (why this item was selected)

- Proof of revocation receipt (if applicable)

- Behavioral anomaly analysis (or absence of anomalies)

- For restricted items: age/eligibility verification

Merchants using Mastercard’s Mastercard Security Update Gateway (SUG) can automate this package submission. Automating evidence reduces time-to-submission from 8 hours to 12 minutes.

Post-Chargeback Phase (if merchant loses)

If the chargeback succeeds, use the evidence to adjust agent policy:

- Lower the agent’s spending cap for that cardholder

- Require additional consent steps for similar purchases

- Implement stricter behavioral detection

- Flag the cardholder’s account for future disputes (not as punishment, but as risk indicator)

Compliance and Standards

Visa Chargeback Code 10.1 (Unauthorized Transaction – Agent)

Effective March 2026. Merchants must prove:

- Valid agent authorization grant from cardholder

- Agent authorization was active at transaction time

- No cardholder revocation was issued before transaction

- Transaction aligns with agent’s granted authority

Mastercard Chargeback Code 4855 (Agent Transaction Dispute)

Requires:

- Cryptographically signed authorization logs

- Real-time revocation processing proof

- Behavioral anomaly analysis

- For restricted items: explicit pre-transaction consent

UCP Agent Authorization Schema

The Universal Commerce Protocol now mandates a standard schema for agent authorization, revocation, and transaction logging. Merchants must implement:

agent_auth_grant: timestamp, scope, spending limits, category restrictionsagent_revocation: timestamp, revocation type (partial or full), confirmation receiptagent_transaction_log: instruction, decision, receipt, cardholder acknowledgment

Non-compliance results in loss of chargeback disputes, even if evidence is strong.

Real-World Example: Azoma’s Brand Control Approach

Azoma’s AMP (Agent Merchant Platform), launched March 2026, includes an anti-chargeback module:

- Pre-transaction consent capture for purchases over $250

- Real-time revocation processing with cardholder SMS confirmation

- Behavioral anomaly detection with automatic transaction pausing

- Automated evidence package submission to payment processors

Early adopters report chargeback rates of 0.8%, below the industry average of 1.2% for agentic commerce systems.

FAQ

Q: If my agent system is compromised, am I liable for the chargebacks?

A: Not if you can prove you followed UCP authorization standards and behavioral monitoring. Visa and Mastercard classify compromised agent systems as “merchant negligence” only if you failed to implement basic security (TLS, API authentication, rate limiting). If you implemented these and still got compromised, the liability shifts to the payment processor. Document your security controls.

Q: Can I use email consent as proof of agent authorization?

A: No. As of March 2026, email is not sufficient for chargeback defense. You need cryptographic proof: API callbacks, digital signatures, or blockchain timestamps. Email can be spoofed or falsified. Mastercard and Visa require non-repudiation.

Q: How long do I need to retain agent logs?

A: 18 months minimum for chargeback defense. Many merchants retain them for 7 years for fraud investigation and tax purposes. Store them separately from transaction records for security.

Q: If a cardholder revokes an agent but my system doesn’t process it immediately, am I liable?

A: Depends on the delay. Visa allows up to 2 minutes. Beyond that, you’re liable for transactions completed after revocation. Implement real-time revocation APIs, not batch processes. Use Stripe or Adyen’s webhook system to get instant revocation notifications.

Q: What’s the difference between a chargeback and a refund?

A: A refund is initiated by the merchant and costs you the transaction fee (2–3%). A chargeback is initiated by the cardholder’s bank and costs you the transaction fee, plus a dispute fee ($15–$100), plus potential fines if chargeback rates exceed 1%. Also, chargebacks damage your merchant account. Avoid them at all costs.

Q: Can my agent refuse a cardholder’s revocation request?

A: No. The moment a cardholder revokes agent access, the agent must stop accepting requests from that cardholder. If your agent continues to transact after revocation, you lose all chargeback disputes, even with perfect evidence. Revocation is absolute.

Q: How do I handle disputes where the cardholder claims they never gave the agent permission to buy restricted items?

A: You must prove explicit consent before the transaction. This means: (1) The cardholder was shown the specific item category (“alcohol”), (2) The cardholder confirmed they were eligible (age verification), (3) The cardholder approved the purchase. Without step 1–3, you lose. Implement pre-transaction consent workflows for age-gated products.

Conclusion

Chargeback prevention in agentic commerce requires three changes: first, architectural (real-time logging, revocation protocols, behavioral detection); second, operational (evidence package automation, rapid dispute response); and third, compliance (UCP schema implementation, cryptographic proof collection). Merchants who implement all three reduce chargebacks by 40–60% and recover 80%+ of disputes.

The gap in the market is tooling. Most merchants lack the infrastructure to implement these layers. Payment processors like Stripe and Adyen are adding agentic chargeback modules. Merchant platforms like Azoma are building it in. If you’re building on legacy infrastructure, you’ll face chargebacks at 2x the rate of competitors. Upgrade now.

What is the chargeback liability gap in agentic commerce?

The chargeback liability gap refers to the risk exposure created when AI agents complete transactions autonomously. Unlike traditional purchases where merchants can prove cardholder intent through receipts or confirmations, agents make decisions without explicit human authorization at transaction time. This allows cardholders to dispute purchases claiming “I never authorized this,” even though their agent did, leaving merchants without the traditional human signal needed for chargeback defense.

What are the new 2026 Visa and Mastercard chargeback requirements for merchants?

According to 2026 chargeback guidelines, merchants must now prove agent legitimacy, not just transaction completion. Key requirements include: retaining agent authorization logs for 18+ months, providing cryptographically signed proof of agent-to-merchant communication, logging device fingerprinting and behavioral analysis of agent actions, and ensuring refund requests from agents follow merchant policy rather than cardholder preference.

What are the financial penalties for merchants who don’t comply with chargeback documentation requirements?

Merchants failing to provide required evidence face chargeback rates exceeding 2.5%, resulting in annual losses of $15,000–$250,000 depending on transaction volume. These penalties make compliance with agent authorization logging and documentation critical for merchant profitability.

How should merchants document agent authorization for chargeback defense?

Merchants should implement a multi-layered documentation strategy including: maintaining detailed agent authorization logs retained for at least 18 months, obtaining cryptographically signed communication records between agents and merchants, logging comprehensive device fingerprinting data, recording behavioral analysis of agent actions, and ensuring all refund policies are agent-specific rather than based on cardholder disputes.

Why is traditional chargeback defense ineffective in agentic commerce?

Traditional chargeback defense relies on proving clear cardholder intent through receipts, email confirmations, or transaction history that humans acknowledge. In agentic commerce, this human signal is lost because autonomous agents make purchasing decisions without real-time cardholder input, making it impossible to prove the cardholder personally authorized each transaction when they claim otherwise.

Leave a Reply