The Silent Killer: Payment Failures in Agent-Driven Transactions

When a customer’s AI shopping agent completes a multi-step purchase—comparing prices, checking inventory, applying discounts, and finalizing payment—a single failure point can cascade into lost sales, orphaned inventory holds, and confused customers. Yet most agentic commerce systems treat payment failures as afterthoughts.

Unlike traditional e-commerce, where a customer sees a red error message and retries, agentic commerce operates in the background. An agent may not immediately signal a failed payment. The merchant’s inventory system may already have decremented stock. The customer’s wallet may have been partially charged. Recovery becomes exponentially harder.

This gap—how to design payment failure handling in agent-driven transactions—remains largely unaddressed in production systems.

Why Agent Payment Failures Are Different

Traditional e-commerce payment failures follow a clear path: customer clicks "pay," payment processor responds (success or decline), customer sees result, and retries if needed.

Agentic commerce inverts this model:

- Async decision-making: An agent may execute multiple sub-transactions (pay supplier, pay fulfillment partner, charge customer) in parallel or sequence, with variable latency.

- No synchronous UI: The customer isn’t watching a progress bar. They’re browsing elsewhere. The agent must detect, interpret, and act on failures autonomously.

- Distributed state: Payment status, inventory, order state, and agent memory may live in different systems. A payment decline in one system doesn’t automatically roll back actions in another.

- Retry ambiguity: Should the agent retry immediately? Wait for customer confirmation? Escalate to a human? Each choice has different cost and UX implications.

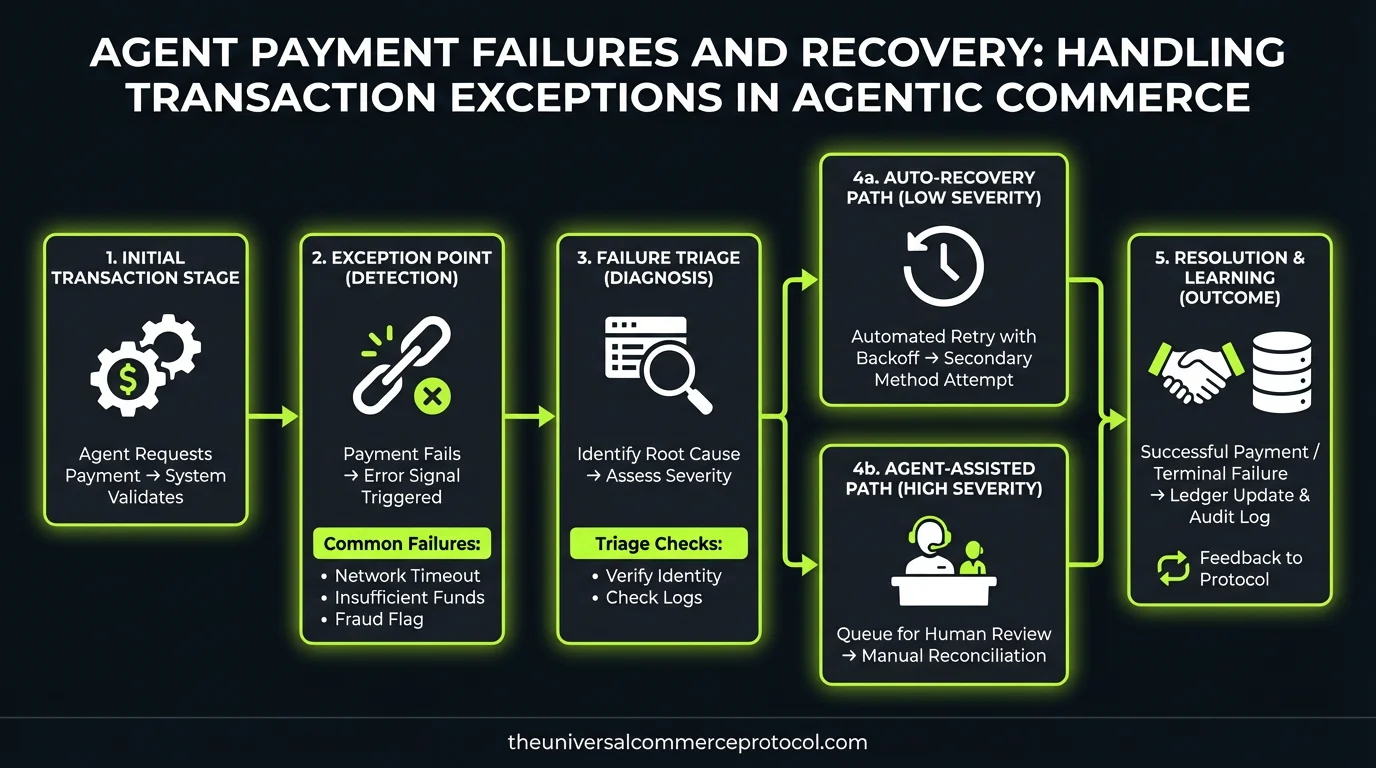

Payment Failure Taxonomy in Agentic Commerce

Category 1: Transient Failures (Recoverable)

Network timeout, processor temporarily unavailable, rate-limit hit. These failures should trigger exponential backoff and retry logic.

Best practice: Implement idempotency keys (tied to the specific transaction attempt, not the customer order) so retries don’t double-charge. Use a dedicated payment_attempt_id separate from order_id.

Category 2: Permanent Failures (Non-Recoverable)

Insufficient funds, card expired, account closed, fraud block. Retrying is pointless.

Best practice: Agent should flag the order as payment_declined, notify the customer with the specific decline reason (if the processor provides it), and ask the agent to offer an alternative payment method or escalate to a human.

Category 3: Ambiguous Failures (Unknown State)

Processor response timeout: payment may have succeeded server-side, but the agent never received confirmation. Charging twice is catastrophic.

Best practice: Query the payment processor’s transaction history before retrying. If the charge already posted, mark the order as paid. If truly unknown after 3 minutes, escalate to merchant support with full transaction logs.

Designing Agent Payment Exception Handlers

1. Explicit Payment State Machine

Define clear, named states:

PAYMENT_PENDING: Agent has requested payment, awaiting responsePAYMENT_PROCESSING: Processor is handling (can last 5–30 seconds)PAYMENT_CAPTURED: Funds confirmed reserved or transferredPAYMENT_SETTLED: Funds fully cleared (end of day)PAYMENT_DECLINED: Permanent reject; customer notifiedPAYMENT_AMBIGUOUS: Unknown state; escalation required

Agent should log every transition with timestamp and processor response code.

2. Timeout Thresholds by Payment Type

Credit card authorization: 10 seconds max. ACH transfer: 2–3 business days. Crypto payment: confirm after 6 blocks.

Agent must know these thresholds and adjust behavior. A 15-second wait for a credit card is a failure; a 4-hour wait for ACH is normal.

3. Inventory Hold Release Policy

If payment fails, when does the agent release the inventory hold?

Recommendation: Release holds immediately on confirmed decline (permanent failure). For transient failures, hold inventory for 5 minutes while agent retries; if still pending after 5 minutes, release and notify customer that the order was cancelled.

This prevents customer frustration (“why is my item out of stock?”) while avoiding double-selling.

4. Customer Notification Strategy

Agent should not silently abandon a failed payment. Instead:

- Permanent decline: Send notification immediately with decline reason and alternative payment options.

- Transient failure with successful retry: Send confirmation of successful payment (no separate decline notification).

- Transient failure + timeout: Send notification that order is pending review, customer will hear back in 24 hours.

Each notification should include a direct link to retry or contact support, not force the customer back to the agent.

Reconciliation and Audit Trails

After a payment failure, the merchant must be able to answer: "Did we charge this customer? Is inventory reserved? What happened?"

Implement:

- Immutable transaction log: Every payment request, response, retry, and state change logged with processor reference ID and timestamp.

- Daily reconciliation job: Compare merchant’s payment records against processor’s settlement report. Flag mismatches (merchant thinks it paid, processor doesn’t have it, or vice versa).

- Agent visibility: When an agent queries "what’s the status of order X?" it retrieves the full transaction history, not just the latest state. This prevents agents from making decisions based on stale data.

FAQ: Payment Failure Handling in Agentic Commerce

Q1: Should an agent ever retry a failed payment without customer consent?

A: For transient failures only (timeout, rate limit), retry automatically with exponential backoff (2s, 5s, 15s, 60s). For permanent declines, always ask the customer first. Store their consent in the agent memory.

Q2: What’s the maximum acceptable payment latency before an agent escalates?

A: 30 seconds for real-time methods (card, bank transfer). If unresolved after 30s, log the ambiguity, don’t retry blindly, and escalate.

Q3: Can an agent use different payment methods if the first fails?

A: Only if the customer has explicitly authorized a fallback method beforehand. Otherwise, ask permission before switching (e.g., "Your card declined; can I try your linked bank account?").

Q4: How do you prevent payment failure from blocking downstream fulfillment?

A: Decouple payment from fulfillment. Mark order as AWAITING_PAYMENT_CONFIRMATION; only move to fulfillment after PAYMENT_CAPTURED. If payment is ambiguous, hold fulfillment and notify the merchant’s operations team.

Q5: Should payment failures be visible in agent traces?

A: Yes, always log payment state transitions to the agent’s execution trace. Merchants and regulators need to audit why an order succeeded or failed.

Q6: How should an agent handle a partial payment (e.g., $50 charged, but $150 order)?

A: Treat as a permanent failure. The processor likely declined the full amount but charged a small amount (e.g., verification hold). Contact the customer immediately, reverse the small charge if possible, and ask for a different payment method. Do not attempt to charge the remaining balance without explicit consent.

Emerging Standards and UCP Relevance

The Universal Commerce Protocol doesn’t yet define a canonical payment failure schema, but Mastercard’s Verifiable Intent framework (integrated with UCP) introduces cryptographic proof of payment authorization. This shifts some failure handling from the agent to the blockchain: a verified intent signature proves the customer authorized the charge, making post-failure disputes easier to resolve.

Merchants implementing agentic commerce should anticipate that UCP 2.0 will include a PaymentException object with standard failure codes (Mastercard’s, ISO 20022, or a new UCP standard). Early adoption of explicit failure handling now will make migration easier.

Key Takeaways

- Payment failures in agentic commerce are not edge cases—they’re a core design problem. Agent payment logic must be explicit, logged, and recoverable.

- Transient failures (timeout, rate limit) warrant automatic retry with backoff. Permanent failures (decline, fraud block) require customer consent and alternative payment methods.

- Inventory holds must be released immediately on confirmed decline to prevent false out-of-stock signals.

- Customer notifications should be sent for permanent failures or extended ambiguity, never for successful retries (which the customer should never see).

- Audit trails are non-negotiable. Merchants must reconcile payment records daily and provide agents with full transaction history, not cached state.

Frequently Asked Questions

Q: How are payment failures in agentic commerce different from traditional e-commerce?

A: In traditional e-commerce, payment failures are synchronous—customers see immediate error messages and can retry. Agentic commerce operates asynchronously in the background, where agents may not immediately signal failures. This creates a critical gap: inventory may already be decremented, customers partially charged, and recovery becomes exponentially harder without proper exception handling.

Q: What cascading problems can result from a single payment failure in agent-driven transactions?

A: A single payment failure can trigger multiple issues simultaneously: lost sales, orphaned inventory holds (stock reserved but not actually sold), partial charges to customer wallets, and confused customers who don’t understand what happened. These problems compound because the agent operates silently without immediate customer visibility.

Q: Why do most agentic commerce systems struggle with payment failure handling?

A: Payment failures are often treated as afterthoughts in agentic systems rather than core architectural concerns. The asynchronous nature of agent decision-making means failures don’t follow the straightforward path of traditional e-commerce, requiring more sophisticated transaction exception handling and recovery mechanisms.

Q: What key factors make payment exception handling critical in agentic commerce?

A: The combination of multi-step agent processes (price comparison, inventory checks, discount application, payment), background operation without immediate customer feedback, and interconnected system states (inventory, wallet, order status) means that payment failures require coordinated recovery across multiple systems to prevent data inconsistency and customer confusion.

Leave a Reply