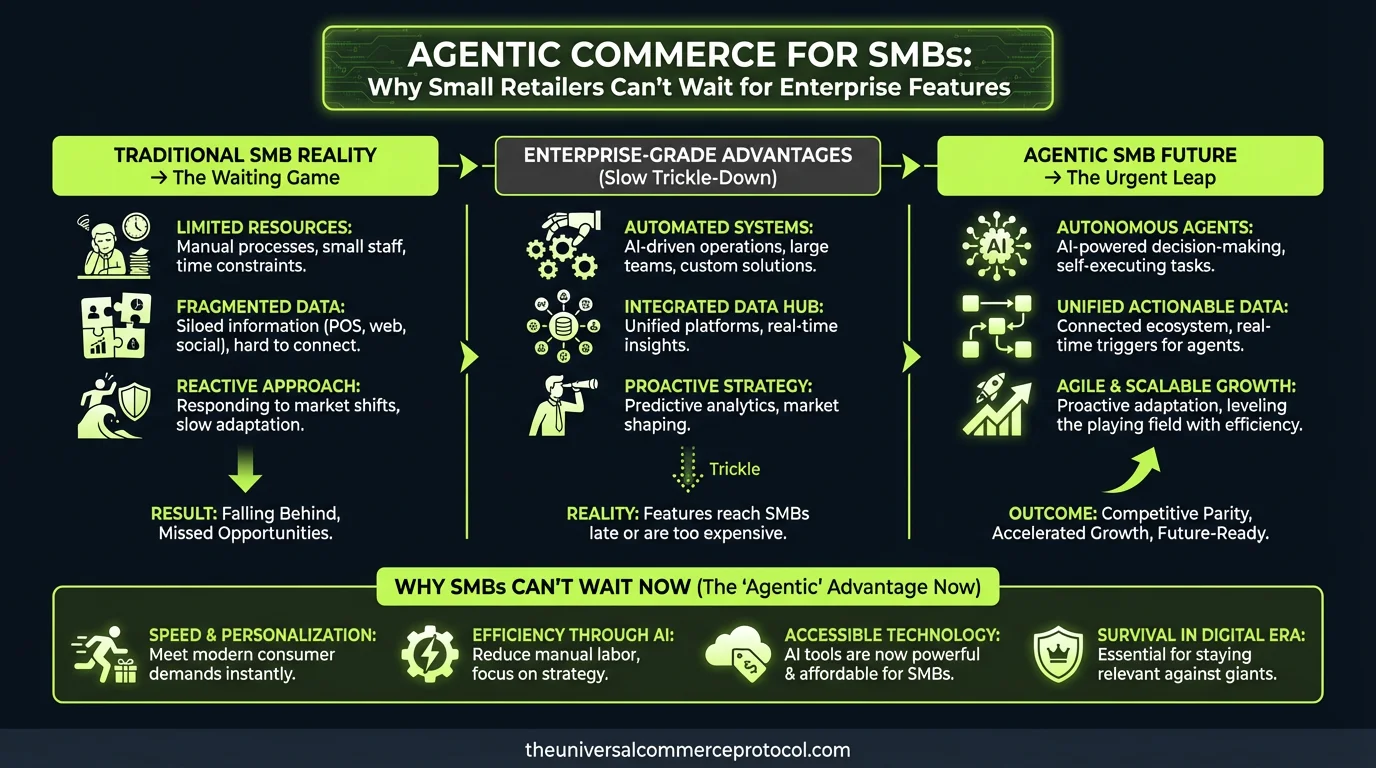

The agentic commerce conversation has been dominated by enterprise plays: Mastercard’s Malaysia pilots, Stripe’s native UCP rails, Shopify’s AI checkout tools. But a critical gap remains unaddressed: how do small and medium-sized businesses (SMBs)—the backbone of e-commerce—actually adopt agentic commerce?

Current coverage assumes merchants have dedicated engineering teams, existing payment infrastructure, and budgets to pilot new protocols. SMBs operate under entirely different constraints.

The SMB Agentic Commerce Gap

Unlike enterprises, SMBs face three structural barriers:

1. Cost of Entry

Agentic commerce requires investment in agent training, observability tooling, and compliance infrastructure. Enterprise merchants can absorb $500K–$2M pilots. SMBs operating on 15–20% margins cannot. No vendor has yet released a sub-$10K starter product for agentic commerce. Shopify’s AI checkout tools remain embedded in higher-tier plans ($299+/month). Stripe’s UCP payment agent APIs require custom integration, not plug-and-play setup.

2. Integration Complexity

SMBs rely on all-in-one platforms (Shopify, WooCommerce, BigCommerce) or lightweight custom builds. They lack the infrastructure to adopt multiple payment agents, fulfillment orchestrators, and fraud detection systems simultaneously. Current agentic architectures require:

- Real-time inventory sync across agents (not built into most SMB platforms)

- Observability dashboards for agent performance (additional vendor lock-in)

- Custom webhook pipelines for cart recovery, returns handling, and subscription management

Enterprises can hire for this. SMBs cannot.

3. Vendor Fragmentation

There is no clear “agentic commerce stack for SMBs.” Merchants must piece together:

- A payment agent (Stripe, PayPal, or Visa’s framework)

- A fulfillment orchestrator (no market leader emerged yet)

- A voice/chat interface layer (Alexa, ChatGPT, or proprietary)

- Fraud detection (Sift, DataBox, or custom ML)

- Returns/subscription management (separate agents)

Enterprises navigate this through procurement teams and system integrators. SMBs have no playbook.

What SMBs Actually Need (And Aren’t Getting)

Plug-and-play agentic checkout. SMBs on Shopify should be able to toggle “agentic mode” and get a pre-trained agent that handles cart recovery, upsells, and payment processing—without coding. This doesn’t exist.

Transparent ROI calculators. Every agentic feature claims revenue lift ($18B in cart recovery potential, $47B in subscription gaps). But where is the SMB case study? A $50K/year vintage apparel brand cannot justify a $30K annual agentic suite without proof of return. No vendor publishes SMB-scale ROI data.

Regulatory clarity for SMBs. Cross-border payment agents require KYC/AML compliance. Agentic fraud detection triggers regulatory reporting. PCI compliance deepens with agent-assisted payment tokenization. SMBs operating in 5+ countries need a simple guide. Current content targets CFOs and technical architects, not SMB owners running operations themselves.

Honest cost models. SMBs need to know: Is agentic commerce a 5-10% revenue lift (worth $5–10K investment) or a 30%+ opportunity (worth $50K+)? At what scale does it pay for itself? When does manual cart recovery become obsolete?

Market Gap: The SMB-Scale Agentic Provider

A significant business opportunity exists for a vendor willing to target SMBs with agentic commerce:

- Positioning: “Agentic checkout for Shopify stores under $5M annual revenue”

- Product: Pre-trained agent APIs + simple dashboard + vendor-agnostic fulfillment hooks

- Pricing: $299–999/month (not $5K+)

- Go-to-market: Shopify App Store, WooCommerce plugin marketplace, case studies from 6-8 figure brands

No such provider exists. Stripe, Shopify, and PayPal are chasing enterprise deals. Smaller players (Saleor, Medusa) lack payment agent infrastructure.

The Real Risk

If agentic commerce remains an enterprise-only tool, SMBs will fall further behind on conversion rate optimization, fraud prevention, and operational efficiency. By 2027, when agent-assisted shopping becomes table-stakes, SMBs will face a two-year integration backlog—and a significant competitive disadvantage.

Current coverage treats agentic commerce as a solved problem. It isn’t. It’s only solved for enterprises. SMBs are still waiting for the first honest, affordable, plug-and-play solution.

That’s the gap that matters most.

“`html

Frequently Asked Questions

Agentic commerce refers to AI-powered agents that can autonomously handle customer transactions and interactions on behalf of merchants. SMBs should care because it can streamline checkout processes, reduce cart abandonment, and improve customer experience—ultimately increasing revenue without requiring large engineering teams to build from scratch.

SMBs face three structural barriers: the high cost of entry (agent training and compliance infrastructure can cost $500K–$2M), lack of dedicated engineering resources to implement and maintain these systems, and tight profit margins (typically 15–20%) that make piloting new technologies financially risky.

Enterprise merchants have dedicated engineering teams, existing payment infrastructure, and large budgets to pilot new protocols, while SMBs operate under entirely different constraints with limited resources. Current agentic commerce solutions are designed for enterprises, leaving SMBs without accessible, cost-effective alternatives tailored to their specific needs and capabilities.

“`

Leave a Reply