The Payment Routing Gap in Agentic Commerce

UCP coverage has focused heavily on inventory sync, error handling, and agent training—but a critical gap exists: how merchants actually orchestrate multiple payment methods within a UCP-enabled checkout flow.

Unlike traditional e-commerce where a customer selects a payment method from a dropdown, agentic commerce agents need to programmatically choose the optimal payment rails based on transaction context: card network availability, regional currency support, fraud signals, interchange costs, and regulatory requirements.

This article addresses the specific mechanics merchants and developers need to implement intelligent payment routing inside UCP.

Understanding UCP Payment Method Orchestration

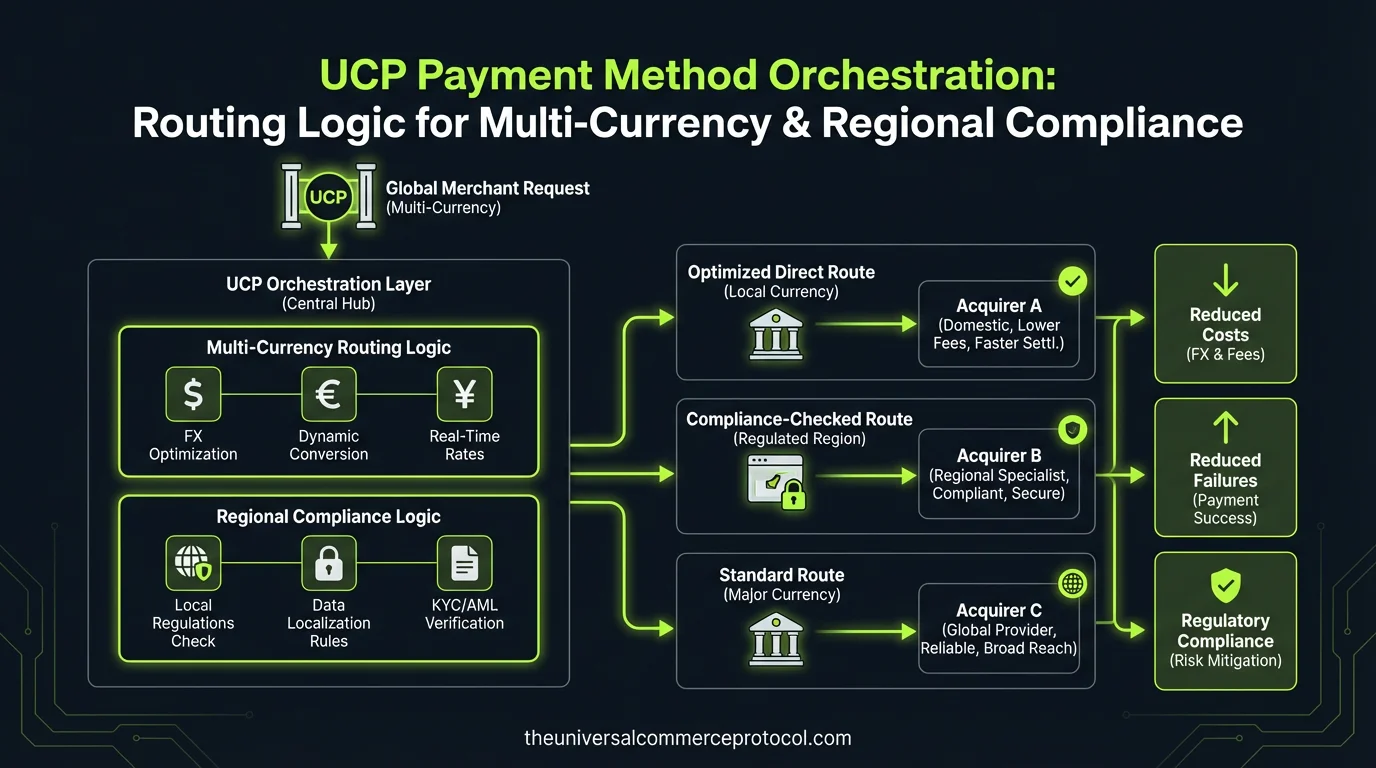

Payment orchestration in UCP differs fundamentally from monolithic payment gateway architecture. Rather than a single payment processor deciding routing, UCP agents integrate with multiple payment providers and apply business logic to select the best option in real time.

The routing decision happens within the agent’s action namespace, not after checkout is complete. This means the agent sees:

- Available payment methods for the customer’s region (determined by IP, billing address, or agent context)

- Real-time interchange costs and processing fees for each method

- Fraud risk scores specific to the transaction

- Currency conversion rates and settlement timelines

- Regulatory restrictions (e.g., SEPA in EU, RBI guidelines in India)

The agent then calls the appropriate UCP payment action with parameters that optimize for merchant KPIs: approval rate, settlement speed, or cost.

Core Routing Patterns

Geographic-Based Routing

A merchant selling globally needs different payment methods active in different regions. A UCP-enabled agent detects the customer’s region (via GeoIP or billing address) and only presents methods legally available and practically used in that market.

Example: An EU customer triggers an agent call to payment.methods.list with region=EU. The UCP action returns only SEPA Direct Debit, EU-licensed card networks, and BNPL providers compliant with PSD2. A customer in Japan receives JCB, convenience store pay, and local digital wallets.

Implementation requires the merchant to maintain a region → approved_methods mapping, ideally stored in a configuration layer that agents reference via a getApprovedMethods(region) helper action.

Cost-Optimized Routing

Different payment methods carry different costs. Card networks charge interchange; ACH and bank transfers are cheaper but slower; BNPL providers take a flat fee upfront.

A merchant optimizing for margin can configure the agent to calculate total cost of each method and rank them. For a $100 transaction:

- Credit card: 2.9% + $0.30 = $3.20

- ACH: $0.50 flat (but 3–5 day settlement)

- BNPL: 3.5% = $3.50 (but faster customer conversion)

The agent can apply different routing rules based on order value, customer segment, or time sensitivity. High-value orders might route to lowest-cost methods; time-sensitive orders to fastest settlement.

Fraud-Adaptive Routing

Payment processors return fraud risk scores. A UCP-enabled agent can use this signal to conditionally route:

- Low risk: Route to lowest-cost method

- Medium risk: Route to method with built-in 3DS (3D Secure) verification

- High risk: Route to method with phone verification, or require additional identity checks before payment

This reduces chargebacks without blocking valid transactions.

Approval Rate Optimization

Some card networks approve more aggressively than others in specific regions. Merchant data science teams can train agents on approval rates per method per geography, then weight routing decisions toward methods with historical approval rates >95%.

A merchant seeing 88% approval on Visa but 94% on Mastercard in a region can bias agent routing toward Mastercard for that region.

Technical Implementation: UCP Payment Action Parameters

UCP payment actions accept parameters that control orchestration:

method_priority: Ordered list of preferred payment methodsregion: Geographic context for compliance filteringcurrency: Required for multi-currency merchants; affects available methods and conversion costsfraud_score: Risk signal from upstream fraud detection; agent uses to select verification levelmax_fee_tolerance: Agent refuses methods exceeding this fee percentagesettlement_requirement: If merchant needs funds within 24 hours, certain methods are excluded

Example payload structure:

payment.process({

method_priority: ["local_bank_transfer", "card", "bnpl"],

region: "EU",

currency: "EUR",

fraud_score: 0.23,

max_fee_tolerance: 0.035,

settlement_requirement: "next_business_day"

})

The UCP orchestration layer then evaluates which methods satisfy all constraints and attempts them in priority order.

Fallback and Retry Logic

Payment orchestration must handle method failures gracefully. If the primary method is declined, the agent should attempt the next prioritized method without asking the customer to re-enter data (unless necessary for compliance).

UCP orchestration supports a retry_config that specifies:

- How many methods to attempt before failing

- Which declines are final (e.g., card stolen) vs. retriable (e.g., issuer timeout)

- Whether to escalate to customer support or offer alternative (e.g., BNPL) if all methods fail

This is distinct from transaction retry logic (covered in prior UCP articles); this is method-level fallback.

Multi-Currency Complications

Merchants operating across currencies face complex routing decisions:

- Local currency processing: Customer sees price in their currency; merchant receives settlement in home currency. Different processors support different currency pairs.

- Dynamic currency conversion (DCC): Some payment methods offer DCC; customer is charged in home currency at a locked-in rate. DCC carries higher fees but improves conversion in some markets.

- Stablecoin and instant settlement: Some UCP-enabled merchants are beginning to accept stablecoins (USDC, USDT) to eliminate FX risk and settlement delay, though regulatory status varies by region.

The agent routing logic must account for these options and their cost/benefit trade-offs.

Regulatory and Compliance Routing

Payment method availability isn’t purely commercial—it’s legal. Examples:

- SEPA: EU merchants must offer SEPA Direct Debit as a low-cost option (PSD2 requirement)

- India: RBI mandates that merchants offer NEFT/RTGS for online transactions; card-only is not compliant

- China: Foreign merchants cannot directly accept UnionPay; must route through licensed acquirers

- Sanctions: Merchants must exclude customers from sanctioned jurisdictions; some payment methods block these automatically

UCP agents must be configured to enforce these constraints, ideally via a compliance rules engine that’s updated as regulations change.

Monitoring and Analytics

Merchants need visibility into how payment routing is performing:

- Approval rates by method: Are certain methods underperforming?

- Cost per method: Is the cheapest method actually cheapest after chargebacks are factored in?

- Settlement velocity: Which methods fund fastest?

- Agent routing decisions: Is the agent prioritizing methods as configured?

UCP orchestration platforms should expose these metrics via dashboards so merchants can tune routing rules based on data.

Common Pitfalls

Over-Routing Complexity: Merchants sometimes configure 10+ payment methods and complex rules, resulting in unpredictable agent behavior and customer confusion. Start with 3–4 methods per region and add complexity only with data.

Ignoring Chargeback Rates: Cheapest method ≠ best ROI. If a method has 1.5% chargebacks and another has 0.2%, the cheaper one may be net more expensive.

Not Testing Regional Variants: A configuration that works in the US may fail in the EU due to different card networks, currencies, or regulations. Test each region’s routing path before live launch.

Hardcoding vs. Configuration: Routing rules should be configurable without code changes. Use feature flags or a configuration service so merchants can adjust rules based on real-time performance.

FAQ

Q: Can a UCP agent change payment method mid-transaction?

Yes, if the first method is declined and a fallback is configured. The agent will attempt the next prioritized method transparently. However, for customer trust, the merchant should log this (e.g., “Primary method declined; attempting your secondary method”) so the customer isn’t surprised by a different charge.

Q: How does UCP handle 3D Secure (3DS) in orchestrated flows?

UCP payment actions can specify require_3ds: true, which forces 3DS verification for that method. The agent can also conditionally require 3DS based on fraud score: low-risk transactions skip 3DS; high-risk transactions require it. This balances security and friction.

Q: Can merchants A/B test payment routing rules in UCP?

Yes. UCP supports configuring different routing rules for different customer segments (e.g., 50% of new customers route to method A, 50% to method B). Metrics are then compared to identify the optimal rule set.

Q: What happens if all payment methods fail?

The agent escalates: either returns an error to the customer (recommending they contact support), or offers an alternative like invoice-based payment or buy-now-pay-later if available. The escalation path is configurable.

Q: Does UCP handle reconciliation across multiple payment methods?

Not natively. UCP handles the payment action and routing; reconciliation is a separate backend concern. However, UCP logs which method was used, settlement ID, and amount, making it easier for merchants to reconcile across their accounting system.

Q: Can UCP agents learn routing preferences from customer history?

Some implementations allow this: if a customer has used method X before with high success, the agent prioritizes X. This requires customer data storage (PII compliance required) and is not a UCP-native feature—it’s a merchant implementation on top of UCP.

Q: How does international expansion affect payment routing?

New markets require new method configurations, regional compliance rules, and often new processor contracts. Merchants expanding should audit their routing rules region-by-region before launch and plan for ongoing updates as local payment preferences shift.

What is UCP Payment Method Orchestration?

UCP Payment Method Orchestration is a system that enables agentic commerce agents to programmatically select the optimal payment method in real-time based on transaction context. Unlike traditional e-commerce where customers manually select a payment method, UCP allows agents to intelligently route payments based on card network availability, regional currency support, fraud signals, interchange costs, and regulatory requirements.

How does payment routing differ in agentic commerce vs. traditional e-commerce?

In traditional e-commerce, customers select a payment method from a dropdown, and a single payment processor handles the transaction. In agentic commerce with UCP, the agent makes the routing decision within its action namespace by analyzing multiple payment providers and business logic factors in real-time, rather than having a single gateway decide routing after checkout is complete.

What factors does UCP consider when routing payments?

UCP payment routing logic considers multiple factors including card network availability, regional currency support, fraud signals, interchange costs, and regulatory requirements. The agent evaluates all these transaction context factors simultaneously to determine the best payment rail for each specific transaction.

Why is payment routing important for merchants using UCP?

Payment routing is critical because it directly impacts transaction success rates, costs, and compliance. Intelligent routing ensures transactions are processed through the most appropriate payment rails based on the customer’s location, currency needs, and risk profile, while also maintaining regulatory compliance across different regions.

What gap did UCP coverage have regarding payment methods?

While UCP coverage focused heavily on inventory sync, error handling, and agent training, it had a critical gap in addressing how merchants actually orchestrate multiple payment methods within a UCP-enabled checkout flow. This article addresses the specific mechanics needed to implement intelligent payment routing inside UCP.

Frequently Asked Questions

What is the Universal Commerce Protocol (UCP)?

The Universal Commerce Protocol (UCP) is an open standard developed to enable AI agents to autonomously conduct commerce transactions across any platform.

How does UCP enable agentic commerce?

UCP provides standardized APIs and protocols so AI agents can discover products, negotiate terms, and complete purchases without human intervention, working across any compatible commerce platform.

Why should businesses implement UCP?

UCP adoption reduces integration costs, opens revenue channels to AI-driven buyers, and future-proofs commerce infrastructure as agentic purchasing becomes mainstream.

Leave a Reply