UCP Compliance & Regulatory Requirements: A Developer’s Checklist for Global Commerce

The Universal Commerce Protocol has accelerated agentic commerce adoption across payment networks, marketplaces, and enterprise platforms. Yet as merchants and developers integrate UCP—especially across borders—a critical gap has emerged: compliance guidance.

While technical integration articles cover API rate limits, error handling, and sandbox testing, almost no published material addresses the regulatory requirements developers must satisfy when building UCP commerce agents. PCI-DSS certification, GDPR data handling, payment processor licensing, and regional restrictions create real legal and financial risk.

This article provides a structured compliance checklist for UCP developers and merchants.

Why UCP Compliance Matters Now

UCP delegates transaction execution to autonomous agents. This fundamentally changes compliance responsibility. In traditional e-commerce, a merchant or payment processor controls the transaction flow. In agentic commerce, the agent decides payment routing, fulfillment timing, and customer data access.

Regulators—including the Federal Reserve (for payment networks), FCA (UK), BaFin (Germany), and the EBA (EU)—have begun issuing guidance on autonomous financial activity. The European Central Bank’s December 2025 consultation on algorithmic decision-making in payments explicitly cited agentic commerce protocols as requiring enhanced oversight.

Payment processors like Stripe and Wizard, both of which now support UCP, publish their own compliance requirements. Your UCP integration must satisfy both the protocol specification and your processor’s regulatory obligations.

PCI-DSS & Payment Data Security

PCI Data Security Standard (PCI-DSS) v4.0, mandatory for all payment processors since March 2025, introduces new requirements for automated payment systems.

What Changed: PCI-DSS v4.0 Section 12.8 now requires documented assessment of automated decision-making systems that affect payment flows. Agents qualify.

Your Compliance Obligations:

- Tokenization: Your UCP agent must never store or transmit full primary account numbers (PANs). All card data must be tokenized via your processor’s payment method endpoint before agent access. Stripe’s UCP integration enforces this; Wizard’s does as well.

- Encryption in Transit: All UCP API calls handling payment data require TLS 1.2 or higher. Validate certificate pinning on client-side implementations.

- Access Controls: Document which agent roles (fulfillment, payment routing, refunds) have access to which payment methods. Use IAM policies to enforce least-privilege access.

- Agent Audit Logging: Log every agent decision involving payment data—routing decisions, failed authorization attempts, method selection criteria. Retain for minimum 1 year (PCI requires 3 months; payment networks often require longer).

- Third-Party Assessment: If your UCP agent integrates with a third-party data enrichment service (fraud scoring, address validation), that vendor must also be PCI-compliant. Verify their Attestation of Compliance (AoC) annually.

Common Failure Point: Developers often cache payment method IDs or processor tokens in agent state to avoid repeated API calls. This violates PCI-DSS Section 3.2.1 (minimize cardholder data). Retrieve tokens only when needed; never persist them in agent memory or logs.

GDPR & Customer Data Rights

If your UCP agent processes transactions for EU customers—or stores any personal data of EU residents—GDPR applies, even if your company is US-based.

Key GDPR Requirements for Agentic Commerce:

- Data Processing Agreements (DPA): Your payment processor (Stripe, Wizard, J.P. Morgan, etc.) must sign a Data Processing Addendum if they access customer data on your behalf. Verify this before deploying agents. Stripe’s Standard Addendum covers UCP; Wizard requires explicit request.

- Algorithmic Transparency (Article 22): EU customers have the right to know if an automated system makes decisions that significantly affect them. Payment routing by an agent may qualify. Your privacy policy must disclose that agent-driven payment selection is in use, and customers must have the right to human review of high-value transactions (typically €500+).

- Data Minimization: Your agent should access only payment and fulfillment data necessary for the transaction. Do not pass customer email, shipping address, or behavioral data to payment routing agents unless required for fraud scoring or compliance. If you do, document the legal basis (usually “legitimate interest” for fraud prevention).

- Retention Limits: Transaction records linked to customer identity must be deleted or anonymized after the legal retention period (typically 7 years for financial records under MiFID II). Agent logs containing customer identifiers fall under this rule.

- Right to Erasure: Implement a process to purge customer data from agent training datasets and cached decision logs within 30 days of request. This is operationally difficult; many companies use synthetic or anonymized data for agent training specifically to avoid this burden.

Practical Implementation: Use UCP’s payment method tokenization to ensure agents never see raw customer identity data. Route only token + transaction amount + merchant ID to the routing agent. This minimizes GDPR exposure because the agent never processes “personal data” as GDPR defines it.

Regional Payment Regulations

United States (Regulation E, NACHA, FinCEN):

- If your agent initiates ACH transfers or wire payments, you must comply with Regulation E (consumer fund transfers). This includes transaction receipt requirements and liability limits for unauthorized transfers. Agents must provide clear pre-authorization for transfers exceeding $100.

- Money transmitter licensing may apply if your agent acts as an intermediary. Stripe and Wizard handle this on your behalf, but you remain responsible if you build custom payment execution agents.

- FinCEN’s travel rule (requiring customer identification for transfers over $3,000) applies to agents routing international payments. Ensure your agent captures and forwards customer identity data as required.

European Union (PSD2 & PSD3):

- Open Banking directive PSD2 requires Strong Customer Authentication (SCA) for most online payments. Agents cannot bypass this. Implement SCA via your processor’s 3D Secure interface; agents should request SCA when needed, not hide it.

- PSD3 (coming 2026) will strengthen agent restrictions further. Expect requirements for real-time monitoring of agent behavior and human approval for high-risk transactions.

UK (Financial Conduct Authority):

- The FCA’s Senior Managers Regime requires individual accountability for automated trading or payment systems. Designate a Senior Manager responsible for your agentic commerce platform and document their oversight process.

Australia (ASIC & ACCC):

- ASIC’s Automated Advice Regime applies if agents make payment method recommendations. Maintain audit trails of agent reasoning (why this payment method was chosen) and make them available to regulators on request.

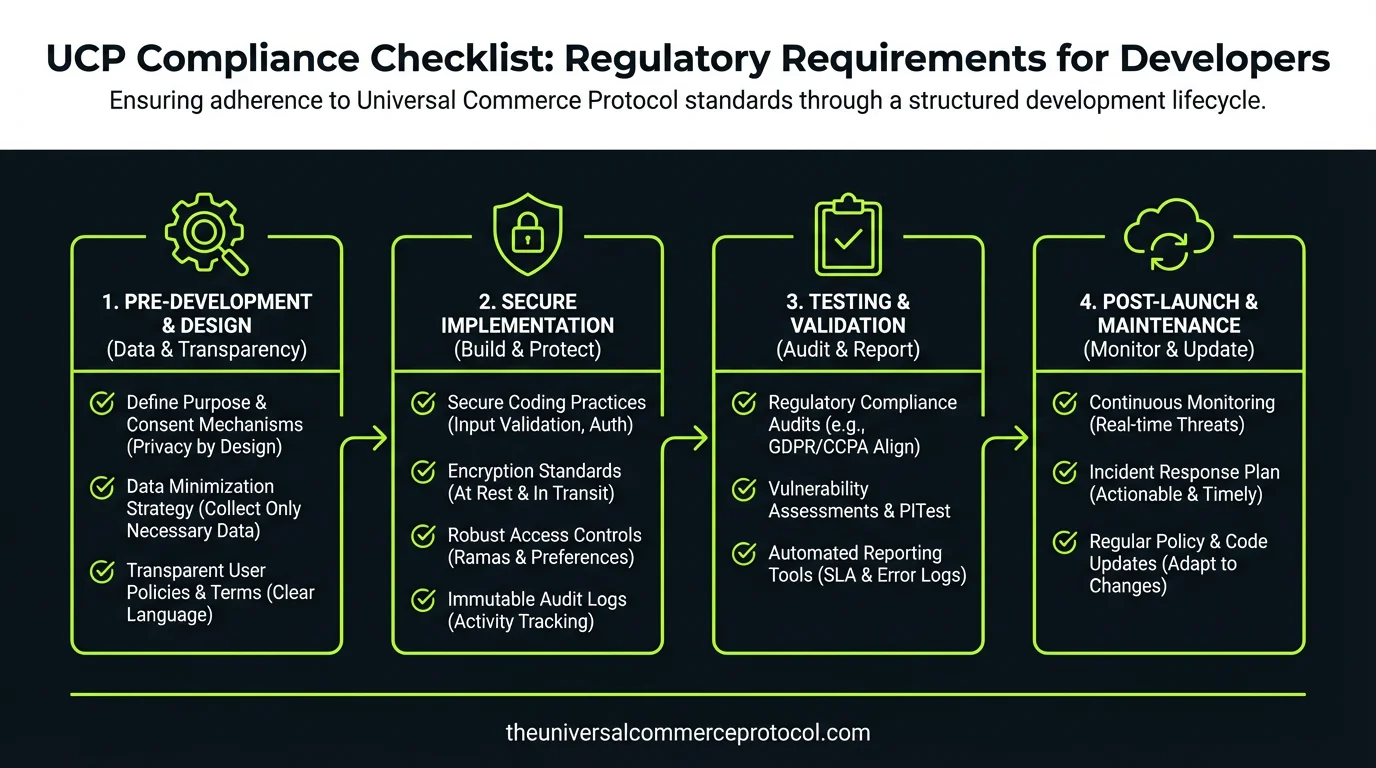

Developer Compliance Checklist

Before Deploying a UCP Agent:

- ☐ Verify your payment processor (Stripe, Wizard, etc.) has signed a DPA or Data Processing Addendum if handling EU customer data.

- ☐ Confirm PCI-DSS v4.0 compliance: tokenization in place, no raw PAN storage, TLS 1.2+ encryption, audit logging enabled.

- ☐ Document which customer data the agent can access. Remove unnecessary fields (email, address, phone) from agent inputs.

- ☐ Implement Strong Customer Authentication (SCA) callbacks. Agents must request SCA when required; do not bypass it.

- ☐ Add agent decision reasoning to transaction logs (e.g., “Routed to Visa due to lower cross-border fee”). Save for minimum 1 year.

- ☐ Set up customer data deletion workflow. Test that customer data removal cascades to agent logs and cached decision models.

- ☐ Configure API rate limiting and monitoring. Alert on anomalous agent behavior (e.g., agent repeatedly selecting the same payment method despite balance failures).

- ☐ Review your privacy policy. Disclose agent-driven payment selection; offer human review option for transactions over your threshold.

- ☐ Engage legal review for any agent behavior that could trigger GDPR Article 22 (automated decision-making). If yes, implement human override.

- ☐ Test UCP integration in compliance sandbox (Stripe Sandbox, Wizard Test Environment) with realistic payment scenarios. Verify compliance logging works.

Frequently Asked Questions

Q: Does PCI-DSS apply to agents if I use tokenized payment methods?

A: Yes, but your exposure is reduced. PCI-DSS v4.0 still requires documented risk assessment of your automated system. Tokenization eliminates the requirement for certain technical controls (like encryption of cardholder data at rest) but not governance. Maintain audit logs and document your assessment.

Q: Can my UCP agent make payment method routing decisions without GDPR consent?

A: Routing decisions based purely on transaction metadata (amount, merchant, payment method availability) generally do not require consent under GDPR. However, if your agent uses customer behavioral data, fraud scoring, or historical purchase patterns to decide routing, you may need to document a “legitimate interest” basis or obtain explicit consent. Stripe and Wizard’s routing agents are designed to minimize data use; clarify with your processor.

Q: What happens if my agent makes a non-compliant payment decision?

A: Liability depends on your processor agreement. Stripe’s UCP terms state that merchants bear liability for agent configuration errors; Wizard has stricter controls and may share liability. Most processors require customers to dispute within 60 days. If an agent violates Regulation E or PSD2, your processor may suspend your integration pending remediation.

Q: Do I need separate compliance for sandbox testing?

A: Sandbox data is typically not regulated (no real customers), but treat sandbox as production for audit logging and PCI controls. This catches compliance bugs before go-live.

Q: Can I train my agent on real transaction history?

A: Not under GDPR without explicit consent and a DPA. Use synthetic or anonymized transaction data for training. Stripe offers anonymized transaction datasets for agent training; ask your processor about similar offerings.

Compliance as Competitive Advantage

As agentic commerce scales, regulators will tighten requirements. Early compliance investment—clear audit trails, data minimization, human-in-the-loop for sensitive decisions—will become table stakes. Companies that embed compliance into agent design now will avoid costly refactoring later.

The most successful UCP implementations treat compliance not as friction, but as design requirement. Your agent’s decision logic, logging, and data access should be built for auditability from day one.

Frequently Asked Questions

What is UCP and why does it require special compliance considerations?

UCP (Universal Commerce Protocol) enables autonomous agents to execute transactions across payment networks and marketplaces. Unlike traditional e-commerce where merchants control transaction flow, UCP delegates this responsibility to autonomous agents. This fundamental shift means agents decide payment routing, fulfillment timing, and customer data access, creating new regulatory responsibilities that differ from conventional commerce platforms.

Which regulatory frameworks apply to UCP compliance?

UCP developers and merchants must address multiple regulatory frameworks including PCI-DSS certification for payment data security, GDPR for customer data handling in EU markets, payment processor licensing requirements, and regional restrictions that vary by jurisdiction. Each framework creates distinct legal and financial risks that must be satisfied during integration.

How does regulatory responsibility change in agentic commerce?

In agentic commerce, compliance responsibility shifts from centralized merchant or payment processor control to a distributed model where autonomous agents make critical transaction decisions. This requires developers to establish governance frameworks, audit trails, and oversight mechanisms to ensure agents operate within regulatory boundaries and maintain compliance across all transaction types.

What should be included in a UCP compliance checklist?

A comprehensive UCP compliance checklist should cover payment security standards (PCI-DSS), data protection regulations (GDPR and regional laws), licensing and registration requirements, agent authorization and governance protocols, transaction audit logging, customer consent mechanisms, and testing procedures in sandbox environments before production deployment.

Why is there a gap between UCP technical documentation and compliance guidance?

Most published UCP materials focus on technical implementation details like API rate limits, error handling, and sandbox testing. However, critical regulatory requirements for cross-border commerce—including payment processor licensing, data residency rules, and regional restrictions—receive minimal coverage, leaving developers without structured compliance guidance for global deployments.

Frequently Asked Questions

What is the Universal Commerce Protocol (UCP)?

The Universal Commerce Protocol (UCP) is an open standard developed to enable AI agents to autonomously conduct commerce transactions across any platform.

How does UCP enable agentic commerce?

UCP provides standardized APIs and protocols so AI agents can discover products, negotiate terms, and complete purchases without human intervention, working across any compatible commerce platform.

Why should businesses implement UCP?

UCP adoption reduces integration costs, opens revenue channels to AI-driven buyers, and future-proofs commerce infrastructure as agentic purchasing becomes mainstream.

Leave a Reply