The Problem: Current agentic commerce posts cover agent refund logic, return windows, and fallback strategies—but none address the critical gap: who decides when an agent can execute a transaction without human approval? As agents become economic actors handling autonomous reversals and multi-step transactions, merchants need tiered approval workflows that balance speed with risk.

What’s Missing: Existing coverage assumes agents either succeed or escalate. Real commerce requires approval gates. A $50 refund? Agent-approved. A $5,000 return on a disputed luxury item? Requires merchant review. A bulk reorder from a VIP customer? Needs finance validation. Today’s posts don’t cover the architecture.

Why Approval Workflows Matter Now

Three recent developments make this urgent:

1. Agent Liability Exposure

The March 13 post on agent liability asks “who pays when AI makes a bad purchase decision?” The answer increasingly is: the merchant does—unless they can prove they had appropriate controls. Approval workflows are that control.

2. Multi-Currency & Dynamic Pricing

The March 12 post on AI agents and multi-currency pricing highlights how agents adjust prices in real-time. A French merchant selling in EUR, GBP, and USD needs approval gates when exchange rate volatility triggers edge-case transactions—otherwise margin erosion compounds.

3. Inventory Desynchronization Risk

The March 12 inventory post shows agents can trigger stock mismatches. An approval layer prevents agents from authorizing returns on zero-stock items or bulk reorders that exceed available inventory.

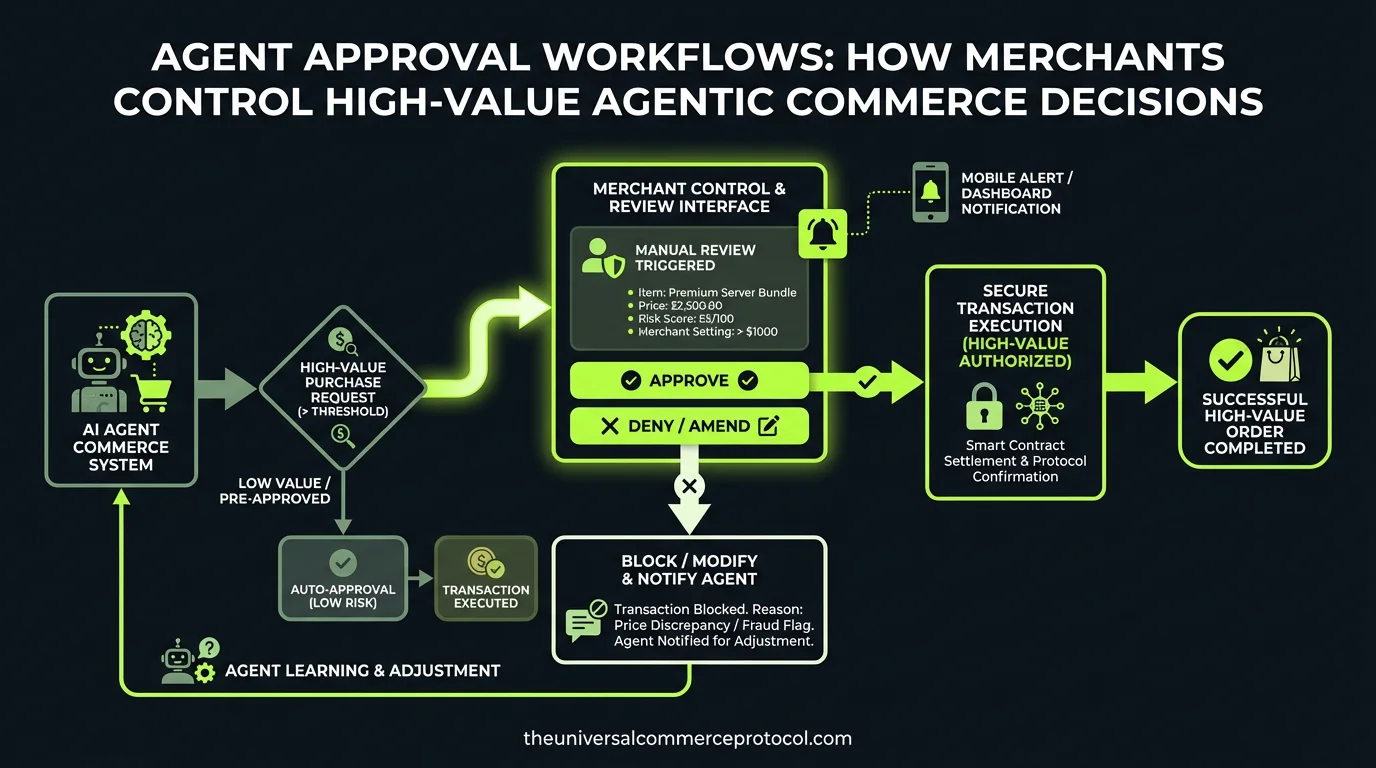

Core Approval Workflow Patterns

Pattern 1: Threshold-Based Gates

Transaction value triggers approval level:

• Under $500: Agent-approved (instant)

• $500–$5,000: Manager approval required (2–4 hour SLA)

• Over $5,000: Executive + Finance sign-off (24-hour SLA)

Merchants using Shopify’s agentic storefronts or JPMorgan/Mirakl’s AI agent checkout should implement role-based approval hierarchies tied to transaction metadata (customer tier, refund reason, payment method).

Pattern 2: Risk-Category Approval

Not all high-value transactions are equal. Approval should also gate by risk:

• Return requests on items >30 days old: Requires proof (image, tracking)

• Refunds to non-original payment method: Requires manual verification

• Bulk orders from new customers: Requires KYC re-check

• Cross-border reversals: Requires compliance review

This decouples decision speed from transaction size—a $100 return from a 5-year customer approves instantly; a $50 refund to an unverified email escalates.

Pattern 3: Conditional Auto-Approval

Merchants can pre-approve agent actions if conditions are met:

• Refund approved if: (customer_ltv > $10k) AND (return_reason == “defective”) AND (refund_amount <= $2,000)

• Return accepted if: (days_since_purchase < 30) AND (condition == “unused”) AND (inventory_available == true)

• Reorder fulfilled if: (customer_status == “vip”) AND (order_history_chargeback == 0) AND (payment_method == “saved_card”)

Claude’s MCP (Model Context Protocol) integration with commerce platforms allows agents to query these rule sets before executing. If conditions fail, agent escalates to human; if met, transaction proceeds with automatic logging for audit.

Technical Implementation for UCP-Compliant Systems

Approval State Machine

Each transaction enters a state chain:

1. Agent evaluates request against approval rules

2. If rules match: auto-approve or conditional-approve

3. If uncertain: queue for human review with reason code

4. Human decision enters audit log (required for UCP compliance)

5. Agent receives approval/rejection and executes or escalates

Merchants building on Google’s UCP framework should model approval as a distinct MCP capability, separate from transaction execution. This allows agents to query approval status without having execution authority.

Audit Trail Integration

Every approval decision must log:

• Agent ID and model version

• Transaction ID, amount, and reason code

• Approval rule applied (or reason for escalation)

• Approver name and timestamp

• Final decision (approved, rejected, escalated)

The March 13 post on cost attribution notes that $2.3M in annual blind spots stem from poor observability. Approval workflows, when properly logged, become your observability layer—CFOs can track which agents generate most escalations, which rule sets are most conservative, and where automation is safe to expand.

Common Implementation Gaps

Gap 1: No Feedback Loop

Agents learn which approvals fail and why. If an agent submits 10 $8,000 refunds and all 10 escalate to finance, the agent should adjust its decision threshold. Most platforms don’t yet feed approval outcomes back into agent fine-tuning.

Gap 2: Slack in Approver Time

A merchant with a 4-hour approval SLA for $500–$5,000 transactions sounds reasonable until midnight hits. Approval workflows need timezone-aware routing and fallback escalation paths (e.g., if manager in timezone A is offline, route to manager in timezone B).

Gap 3: No Approval Expiry

An approval issued at 3 PM is valid for a transaction at 5 PM—but is it valid at 3 PM the next day? Inventory, pricing, and customer risk profiles change. Approvals should have TTLs (time-to-live), forcing re-evaluation if execution is delayed.

FAQ

Q: Can agents approve other agents’ requests?

A: Not in current production systems. Agent-to-agent commerce exists (per March 13 post), but B2B order flows still require human validation. This is an emerging use case—two supply-chain agents negotiating bulk terms will eventually need self-approval rules, but that’s 2026-27 at earliest.

Q: Should approval workflows be part of UCP spec?

A: Partially. UCP governs data format and protocol, not business logic. Merchants define their own approval rules; the UCP layer should standardize how agents query approval status and log decisions. Mastercard/Google’s trust layer (March 13) hints at standardizing approval requests across networks.

Q: What if an agent executes a transaction without approval?

A: This is your insurance edge case (per Agent Liability post, March 13). Approval workflow logs prove you had controls in place. If an agent acts outside those controls, you have evidence of the breach and can demonstrate negligence was agent-side, not merchant-side. Documentation is liability protection.

Q: Can approval workflows reduce cart abandonment?

A: Yes, indirectly. The March 13 cart abandonment post cites customer friction as a cause. Agents handling pre-approved refunds or instant returns (for VIP customers) reduce abandonment. Conversely, requiring approval on every small action delays completion and increases abandonment. The goal is hidden approvals—customer sees instant action, merchant sees approval logging behind the scenes.

Q: How do approval workflows interact with agent retry logic?

A: Separate concerns. Retry logic (March 13 post) handles technical failures (payment processor timeout). Approval workflows handle business decisions (should this refund be allowed?). A refund can retry 3 times, then escalate to approval if all retries fail. Or it can be approved, retry once on execution failure, then fall back to manual payment reversal.

Next Steps

Merchants deploying agentic commerce should:

1. Audit current escalation paths: Where do today’s rule-based systems escalate? Mirror those thresholds into agent approval rules.

2. Define approval roles: Who approves what? Build matrix (role × transaction type × value range).

3. Set SLAs for each tier: When approval is needed, how long can customer wait? Price that latency into your UX.

4. Log everything: Make approvals observable (tie into cost attribution and hallucination detection from earlier posts). Use logs to optimize rules over time.

5. Test edge cases: What if approver is offline? What if rule engine is slow? Build fallbacks.

Approval workflows are the control layer that makes “agents become economic actors” (March 13) sustainable. Without them, you’re liable.

Frequently Asked Questions

Q: What is an agent approval workflow in agentic commerce?

A: An agent approval workflow is a tiered system that determines when autonomous agents can execute commerce transactions without human intervention. It sets thresholds based on transaction value, type, and risk level—allowing agents to auto-approve low-risk transactions (like a $50 refund) while escalating higher-risk decisions (like a $5,000 disputed return) to merchant review. This balances operational speed with financial risk management.

Q: Why do merchants need approval workflows if agents are supposed to be autonomous?

A: Approval workflows protect merchants from liability exposure. As agents become economic actors handling refunds and multi-step transactions, merchants are legally responsible for poor decisions unless they can demonstrate appropriate controls were in place. Approval gates serve as that documented control mechanism, reducing liability and preventing unauthorized financial commitments.

Q: How should approval thresholds be set?

A: Thresholds should be tiered based on multiple factors: transaction value (e.g., $0-100 auto-approved, $100-1,000 requires manager review, $1,000+ requires executive approval), transaction type (routine refunds vs. disputed claims), customer status (VIP vs. new customers), and currency/exchange rate volatility. Dynamic pricing and multi-currency transactions may require lower approval thresholds due to margin erosion risks.

Q: What types of transactions typically require merchant approval?

A: High-value disputes, bulk reorders from high-value customers requiring finance validation, transactions involving exchange rate volatility in multi-currency environments, returns on luxury or high-ticket items, and any transaction outside normal parameters should require merchant approval. Low-risk transactions like standard refunds within policy windows can typically be agent-approved.

Q: How do approval workflows handle real-time decisions in fast-moving commerce?

A: Effective workflows use automated routing to speed up approvals—pre-approved templates for common scenarios, escalation APIs that alert relevant teams instantly, and conditional logic that routes decisions to the right stakeholder (inventory manager for stock issues, finance for currency edge-cases, customer service for disputes). This maintains speed while keeping humans in control of high-risk decisions.

Leave a Reply