When a commerce AI agent reaches checkout, it doesn’t just process a transaction—it makes a strategic choice about how that transaction flows through payment rails. This decision directly impacts approval rates, merchant fees, chargeback risk, and customer experience.

Yet the site has covered payment failures, chargeback prevention, and checkout flows without addressing the upstream problem: how should an agent decide which payment method to offer or prefer?

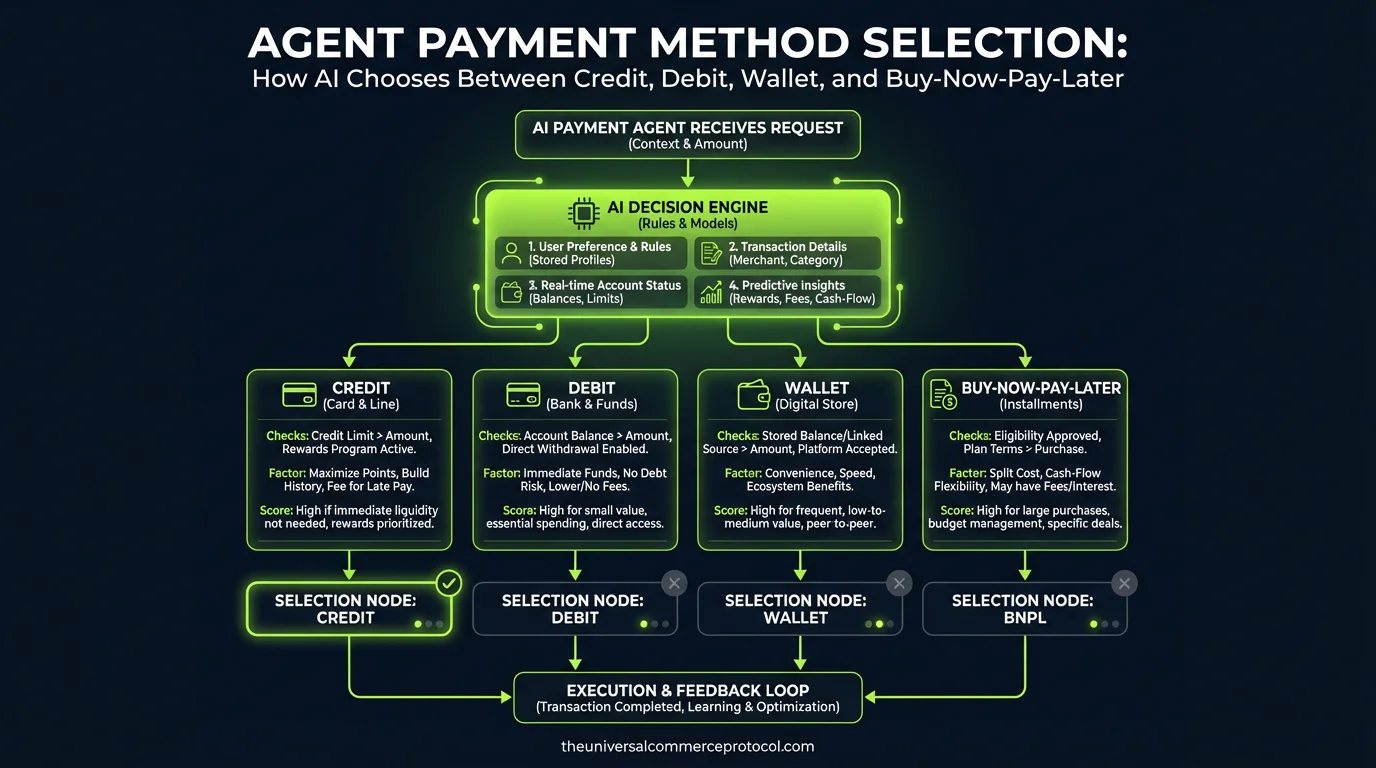

The Payment Method Selection Problem

Traditional e-commerce presents customers with options and lets them choose. Agentic commerce inverts this: the agent must decide, often in milliseconds, which method to attempt first—and how to handle decline scenarios.

This choice isn’t obvious. A $50 order on a consumer’s debit card has different approval odds, fees, and dispute mechanics than the same order via BNPL or a digital wallet. An agent trained only on conversion rate may pick the method with highest approval likelihood, ignoring merchant margin erosion from BNPL fees (3–8% in many markets) or the hidden cost of deferred settlements.

Payment Rail Economics: What Agents Need to Know

Credit Card Networks (Visa/Mastercard/Amex): Highest approval rates (95–98% for prime customers), but interchange fees run 1.5–2.9% plus assessment fees. Chargeback windows extend 120 days, creating long-tail dispute tail risk. Agents should prioritize credit for high-confidence transactions where customer identity is verified.

Mastercard’s March 2026 trust layer initiative (announced with Google) introduced optional agent-sourced confidence scoring. Early data from beta merchants shows agents trained to declare confidence levels above 0.92 see 4–6% lower chargeback rates when Mastercard routes transactions through expedited settlement.

Debit Cards: Lower approval rates (88–92%) due to insufficient-funds declines, but dramatically lower chargeback risk (15–20 day windows, lower dispute rates overall). Fees run 0.5–1.2%. Best for known-good customers or repeat purchases where the agent has transaction history.

Digital Wallets (Apple Pay, Google Pay, PayPal): Approval rates vary by issuer (90–96%), but the wallet provider absorbs initial liability. Transaction fees average 2.2–2.9%. Critical advantage: wallets tokenize the underlying payment method, so an agent attempting an Apple Pay transaction doesn’t expose the raw card number—reducing fraud surface. Recommended as default for unknown customers or high-fraud verticals (fashion resale, luxury goods).

Buy-Now-Pay-Later (Affirm, Klarna, Afterpay): Highest approval rates in their cohorts (92–96% within risk bands they accept), but merchant fees are brutal: 3–8% per transaction, plus 0.5% settlement fees. BNPL works for cart values $50–$500; agents shouldn’t offer BNPL for sub-$30 orders (fee-to-transaction ratio becomes irrational). BNPL also fragments the merchant’s settlement timeline—some providers pay in 24 hours, others in 3–5 days, creating reconciliation complexity that impacts cost attribution models.

Shopify’s March 2026 ChatGPT integration includes optional BNPL promotion, but only for baskets flagged as “replenishment” or “repeat customer.” This signals that agents should use behavioral signals, not just transaction size, to decide.

Agent Decision Frameworks: Three Approaches

Approval-First Strategy: Agents rank payment methods purely by approval likelihood. For a new customer with an unknown issuer, the agent tries: Apple Pay → Google Pay → Debit → Credit → BNPL. Fast transaction completion, high UX satisfaction, but often leaves money on the table (high-fee BNPL attempts when credit would have approved).

Margin-Optimized Strategy: Agents rank by merchant net revenue after all fees. Credit (1.5–2.9% cost) ranks above BNPL (3–8% cost) for the same approval likelihood. This approach requires the agent to know merchant’s interchange pricing in real-time—not always available at API call time. JPMorgan and Mirakl’s March 2026 partnership includes a “merchant fee transparency service” that agents can query to make per-transaction decisions; early adopters report 40–60 bps margin improvement per transaction.

Risk-Adjusted Strategy: Agents model approval + chargeback + fraud probability together, weighting by customer signal quality. If the agent has high-confidence identity verification (phone verified, email verified, prior purchase history), it prefers credit (low dispute risk). If confidence is low (new account, suspicious geo-velocity), it prefers wallet (issuer liability) or BNPL (provider handles fraud screening). This requires agents to maintain a live risk score, updated in real-time from upstream fraud detection.

Implementing Agent Payment Selection Logic

Input Requirements: The agent needs four data sources:

- Customer risk profile (confidence score, fraud signals, prior transaction history)

- Merchant fee matrix (cost per method, settlement terms, chargeback reserves)

- Card network response times and approval heuristics (varies by issuer, geog, time-of-day)

- Inventory and fulfillment constraints (BNPL preferred for pre-orders or long fulfillment windows; credit for same-day delivery)

Decision Checkpoint: The agent should make this choice at cart finalization, not at payment submission. This allows the agent to:

- Decline the purchase if required payment method isn’t available (e.g., BNPL-only customer in a market where the merchant hasn’t enabled it)

- Suggest alternative products if the payment method has cart-size constraints

- Adjust fulfillment commitments based on settlement speed (BNPL 5-day settlement requires conservative inventory deduction)

Fallback Orchestration: Agents should attempt payment methods in a prioritized chain, but with intelligent retry logic:

- If credit card declines with code 51 (insufficient funds), immediately escalate to debit or wallet—don’t retry credit 3 times

- If wallet fails with authentication error, fall back to card-on-file, not BNPL (friction increase too high)

- If all primary methods exhaust, offer BNPL as explicit opt-in before declining the cart

The site’s March 13 post “Agent Fallback Strategies” covers detection and recovery, but doesn’t address the upstream decision of which method to try first—a gap this article fills.

Real-World Trade-Offs

Walmart’s adoption of Google’s UCP (announced March 13) includes a disclosed payment-selection layer: agents attempt Google Pay first (Walmart’s preferred method, lowest settlement friction), then Walmart credit card, then external cards, then BNPL. This isn’t random—it’s optimized for Walmart’s margin, not customer convenience. Competitors should model their own priority based on their interchange agreements and BNPL contracts.

One merchant reported that switching from approval-first to margin-optimized logic increased average transaction fees from 2.1% to 2.3%, but absolute margin improved 85 bps because fewer BNPL transactions were attempted on high-confidence customers. The tradeoff: approval rate dropped 0.6% (from 96.2% to 95.6%), but only among the highest-risk cohort.

FAQ

Q: Should agents offer BNPL to all customers, or restrict it?

A: Restrict it. BNPL makes sense for carts $50–$500 and customers flagged as younger (18–35) or first-time buyers. For repeat customers with known payment methods, BNPL is pure fee drag. For sub-$30 orders, the fee-to-value ratio is negative.

Q: How often should agents re-evaluate their payment method ranking?

A: Per transaction. Customer risk profile changes per session; merchant fees may change quarterly or when new integrations launch. Cache rankings for no more than 60 seconds to avoid stale signals.

Q: What if the customer’s preferred method isn’t available?

A: Agents should surface the constraint upfront (“Apple Pay not available in your region”) rather than attempting payment and failing. This requires agents to know geopolitical payment restrictions—a common gap.

Q: Does payment method selection impact agent liability?

A: Potentially. If an agent chooses a method that fails or disputes at higher rates than an alternative, and the merchant can prove the agent had access to that signal, it could affect liability allocation. However, there’s no settled case law yet. See “Agent Liability & Insurance” (March 13) for the broader framework.

Q: Should merchants publish their payment method rankings to customers?

A: Not the full ranking, but transparency helps. Shopify’s ChatGPT integration shows customers why a particular method was chosen (“Using Apple Pay for faster checkout”), improving trust. See “Agent-to-Consumer Communication” (March 13).

Q: How do subscription or recurring charges affect method selection?

A: Subscription agents should prefer methods that support tokenization and stored credentials: cards on file, digital wallets, or BNPL with renewal terms. Credit cards are best for recurring (lowest chargeback risk on known intervals), but BNPL with explicit renewal consent is increasingly supported. Don’t attempt debit for recurring charges without explicit customer approval—insufficient-funds retries tank CLTV.

Frequently Asked Questions

Q: How do AI agents decide which payment method to use at checkout?

A: AI agents make strategic payment method decisions in milliseconds based on multiple factors including approval rates, merchant fees, chargeback risk, and customer experience. Rather than presenting options to customers like traditional e-commerce, agentic commerce has the AI select the optimal payment method automatically, considering the specific transaction context.

Q: What are the key differences between payment methods from an AI perspective?

A: Different payment methods have distinct economics and risk profiles. Credit cards, debit cards, digital wallets, and BNPL options each carry different approval odds, fee structures, settlement timelines, and dispute mechanics. For example, BNPL typically charges merchants 3–8% in fees, while credit card networks have different approval rates and chargeback risks compared to debit or wallet-based payments.

Q: Why can’t AI agents just optimize for approval rates when selecting payment methods?

A: Optimizing solely for approval rates ignores critical business factors like merchant margin erosion, settlement delays, and dispute costs. An agent focused only on conversion may select BNPL methods with high approval likelihood, but these incur substantial fees (3–8%) that reduce profitability. A well-designed agent must balance approval rates with merchant economics and risk factors.

Q: How does payment method selection impact merchant fees and profitability?

A: The choice of payment method directly affects the merchant’s bottom line through processing fees, chargeback liability, and settlement timing. BNPL options carry higher merchant fees, while different card networks and debit transactions have varying fee structures. AI agents should weigh these costs against approval rates to maximize overall transaction value.

Q: What should happen when an AI agent’s first payment method choice is declined?

A: The agent needs a strategic fallback approach to handle decline scenarios. Rather than having predetermined backup methods, the agent should evaluate remaining payment options based on the same factors—approval likelihood, fees, and risk—adjusted based on why the initial method failed. This requires understanding decline codes and payment rail mechanics.

Leave a Reply