Understanding the Agent Payments Protocol Within UCP

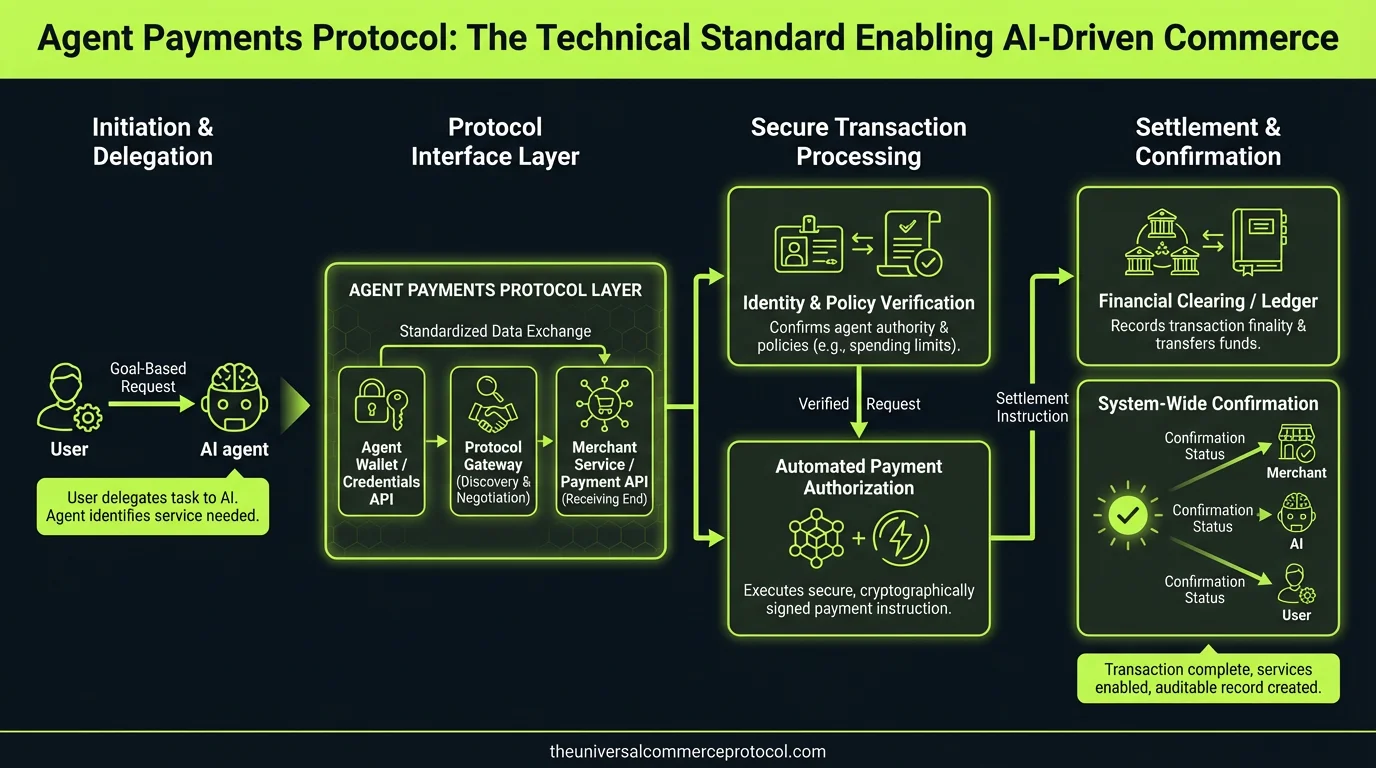

The Universal Commerce Protocol (UCP) establishes a comprehensive framework for agentic commerce, but its success fundamentally depends on a robust payments layer. The Agent Payments Protocol operates as the settlement and authorization backbone within UCP, enabling autonomous agents to conduct transactions with the same security guarantees and regulatory compliance required in traditional commerce systems. Unlike conventional payment processors that assume human merchants and consumers, the Agent Payments Protocol must accommodate machine-to-machine transactions while maintaining PCI-DSS compliance, fraud detection, and settlement integrity.

At its core, the Agent Payments Protocol sits between three critical infrastructure layers: the commerce orchestration layer (where UCP routing occurs), the authorization and settlement layer (connecting to Visa, Mastercard, ACH networks), and the distributed ledger or custody layer (where cryptographic proof of payment is maintained). This positioning requires the protocol to translate between incompatible standards—converting API-first agent requests into legacy payment network messages while simultaneously maintaining real-time settlement guarantees.

Technical Architecture: How Agent Payments Protocol Integrates with UCP

The Payment Authorization Stack

The Agent Payments Protocol implements a multi-layer authorization model that differs fundamentally from traditional three-party (merchant-acquirer-issuer) payment systems. In agentic commerce, authorization must account for agent delegation, principal liability, and autonomous decision-making constraints.

- Agent Identity Verification Layer: Agents must present cryptographic credentials (typically Ed25519 or ECDSA key pairs) that prove authorization from a principal (human merchant or business entity). This layer integrates with OAuth 2.0 and OpenID Connect standards but extends them with agent-specific claims including spending limits, transaction categories, and temporal constraints.

- Transaction Authorization Layer: Each transaction request includes UCP-specific metadata: product catalog references (using GS1 or proprietary SKU systems), merchant category codes (MCCs), and agent decision rationale. The protocol validates that the transaction falls within the agent’s delegated authority before submitting to payment networks.

- Network Authorization Layer: The protocol translates agent requests into ISO 20022 messages for ACH, ISO 8583 for card networks, or real-time payment protocols like FedNow (Federal Reserve) or The Clearing House RTP. This translation layer maintains semantic equivalence—ensuring that UCP-level transaction details map correctly to legacy payment network requirements.

Settlement and Custody Models

The Agent Payments Protocol supports multiple settlement architectures, each with different security and finality guarantees:

- Traditional Acquiring Bank Settlement: Agents submit transactions through established payment processors like Stripe, Square, or Adyen. The protocol wraps agent credentials and transaction data in a format compatible with these processors’ APIs, enabling agents to leverage existing merchant acquiring infrastructure. Settlement occurs through traditional T+1 or T+2 cycles.

- Real-Time Payment Settlement: For higher-value or time-sensitive transactions, agents can route payments through FedNow or RTP networks, achieving settlement finality within seconds. The Agent Payments Protocol implements the SWIFT gpi (global payments innovation) framework for cross-border transactions, enabling agents to settle internationally with transparent fee structures and delivery-versus-payment (DvP) guarantees.

- Blockchain-Based Settlement: For decentralized commerce scenarios, the protocol supports settlement on public blockchains (Ethereum, Solana) or permissioned ledgers (Hyperledger Fabric, Corda). In these models, agents submit transactions as smart contract calls, with settlement finality determined by blockchain consensus rules. The protocol implements atomic swaps and hash time-locked contracts (HTLCs) for cross-chain settlement.

Key Technical Components of the Agent Payments Protocol

Agent Credential Management

Agents require cryptographically verifiable credentials that establish their right to execute transactions on behalf of a principal. The Agent Payments Protocol implements a credential model based on W3C Verifiable Credentials (VC) standard, extended with commerce-specific attributes:

- Issuer: The principal (merchant, business, or individual) delegating payment authority

- Subject: The agent (AI system, bot, or autonomous service) receiving payment authority

- Claims: Specific transaction permissions including maximum transaction amount, allowed merchant categories (via MCC codes), allowed currencies, and temporal validity windows

- Proof: Cryptographic signature from issuer, verifiable by payment processors and settlement networks

These credentials integrate with existing KYC/AML infrastructure through APIs provided by providers like Onfido, IDology, and LexisNexis. When an agent initiates a transaction, the protocol automatically includes credential proof alongside transaction details, enabling payment processors to verify agent authorization without requiring human intervention.

Transaction Routing and Optimization

The Agent Payments Protocol implements intelligent routing logic that selects the optimal payment network based on transaction characteristics:

- Card Networks (Visa, Mastercard, Discover): Optimal for consumer-to-business transactions, cross-border payments, and scenarios requiring chargeback protection. The protocol implements EMV 3-D Secure 2.x for authentication, reducing fraud while enabling frictionless agent-initiated transactions.

- ACH (Automated Clearing House): Cost-effective for business-to-business transactions and recurring payments. The protocol supports both debit and credit transfers, with the ability to implement CCD (Cash Concentration or Disbursement) and CTX (Corporate Trade Exchange) formats for complex B2B scenarios.

- Wire Transfers (SWIFT): For high-value international transactions requiring immediate settlement. The protocol implements SWIFT MT103 message format with embedded UCP transaction metadata, enabling receiving banks to automatically reconcile payments with commerce orders.

- Real-Time Payment Networks: The protocol prioritizes FedNow, RTP, and international equivalents (SEPA Instant, Faster Payments) for transactions under $100,000 where real-time settlement is critical to commerce flow.

Fraud Detection and Risk Scoring

Autonomous agents present novel fraud vectors that traditional payment processors weren’t designed to detect. The Agent Payments Protocol implements a multi-signal risk assessment engine that evaluates:

- Agent behavioral consistency (comparing current transaction to historical agent transaction patterns)

- Principal account health (detecting compromised merchant accounts that might be issuing fraudulent agent credentials)

- Network-level anomalies (detecting coordinated fraud across multiple agents or principals)

- Transaction velocity (identifying unusual acceleration in transaction frequency or value)

- Geolocation inconsistencies (flagging transactions inconsistent with agent deployment geography)

This risk scoring integrates with third-party fraud detection services like Kount, Ravelin, and Sift Science, which have begun implementing agent-specific detection models trained on agentic commerce transaction data.

Integration with Existing Payment Infrastructure

Backward Compatibility with Legacy Systems

A critical design principle of the Agent Payments Protocol is compatibility with existing payment infrastructure. Rather than requiring wholesale replacement of merchant acquiring systems, the protocol implements adapters that translate between UCP-native formats and legacy payment processor APIs.

For example, when an agent needs to process a payment through Stripe, the protocol converts the UCP transaction request into a Stripe Payment Intent, automatically mapping UCP-specific metadata (agent identity, delegation proof, transaction category) into Stripe’s metadata fields and custom attributes. This enables merchants to adopt agentic commerce without replacing their existing payment infrastructure.

PCI-DSS Compliance and Tokenization

The Agent Payments Protocol implements tokenization at the protocol level, ensuring that sensitive payment data (card numbers, bank account details) never passes through agent systems. When a principal first authorizes an agent, the protocol creates a payment token that represents the underlying payment method without exposing sensitive details.

All subsequent agent transactions reference this token rather than actual payment credentials. This approach maintains PCI-DSS compliance (agents can operate in non-DSS-compliant environments) while enabling agents to execute transactions without access to raw payment data. The protocol implements the ISO/IEC 11571 standard for payment token management, ensuring interoperability across payment processors.

Real-World Implementation: Agent Payments Protocol in Practice

Consider a supply chain scenario where an AI procurement agent manages inventory for a retail chain. The agent continuously monitors stock levels and automatically purchases inventory from approved suppliers. The Agent Payments Protocol enables this workflow:

- The retail company issues a W3C Verifiable Credential to the procurement agent, granting authority to execute purchases up to $50,000 per transaction from pre-approved suppliers.

- When inventory drops below threshold, the agent evaluates multiple suppliers and selects the optimal option based on price, delivery time, and quality metrics.

- The agent initiates a payment through the Agent Payments Protocol, which routes the transaction through the ACH network (cost-effective for B2B) with a 2-day settlement window.

- The protocol automatically submits the agent’s credential proof to the agent’s bank, which verifies authorization and clears the transaction.

- Upon settlement, the protocol generates a cryptographically signed receipt that serves as proof of payment for audit and reconciliation purposes.

This workflow executes entirely without human intervention, yet maintains full auditability and regulatory compliance through the Agent Payments Protocol’s credential and settlement mechanisms.

Emerging Standards and Future Evolution

The Agent Payments Protocol continues to evolve alongside broader payment industry standards. The ISO 20022 migration (replacing ISO 8583 for card networks and ISO 20022 XML for all payment types) will significantly simplify agent-to-payment-network translation. Additionally, emerging standards like CBDC (Central Bank Digital Currency) infrastructure from the Federal Reserve and ECB will create new settlement pathways that the protocol will need to accommodate.

The protocol is also incorporating emerging cryptographic standards from NIST, including post-quantum algorithms that will maintain security as quantum computing capabilities advance. This forward-looking approach ensures that agent credentials issued today will remain cryptographically valid in the post-quantum era.

FAQ: Agent Payments Protocol and UCP

How does the Agent Payments Protocol differ from traditional payment APIs like Stripe or Square?

Traditional payment APIs assume a human merchant initiating transactions through a web or mobile interface. The Agent Payments Protocol is purpose-built for autonomous agents, implementing cryptographic delegation (agents must prove authorization from a principal), real-time risk assessment specific to agent behavior, and support for multiple settlement networks (not just card networks). Additionally, the protocol standardizes agent-to-payment-network communication, enabling agents to switch between payment processors without code changes.

What happens if an agent’s credentials are compromised?

Principals can revoke agent credentials in real-time through the protocol’s credential management interface. Upon revocation, all subsequent transactions from that agent are rejected at the authorization layer before reaching payment networks. The protocol also implements transaction monitoring that can detect suspicious agent behavior and automatically revoke credentials if anomalies exceed configured thresholds.

Can the Agent Payments Protocol support international transactions?

Yes. The protocol implements SWIFT gpi for international wire transfers, supports SEPA for Eurozone transactions, and includes adapters for regional payment networks (China’s CIPS, India’s UPI). Currency conversion is handled through real-time FX APIs from providers like OFX and Wise, with FX rates locked at transaction initiation to eliminate rate volatility risk.

How does settlement finality work in the Agent Payments Protocol?

Settlement finality depends on the underlying payment network: ACH transactions achieve finality after 1-2 business days, real-time payment networks (FedNow, RTP) achieve finality within seconds, and blockchain-based settlement achieves finality after blockchain confirmation (typically 12-60 seconds on Ethereum). The protocol exposes settlement finality guarantees to agents and merchants, enabling them to make informed decisions about which settlement network to use for each transaction.

Frequently Asked Questions

What is the Universal Commerce Protocol (UCP)?

The Universal Commerce Protocol (UCP) is an open standard developed to enable AI agents to autonomously conduct commerce transactions across any platform.

How does UCP enable agentic commerce?

UCP provides standardized APIs and protocols so AI agents can discover products, negotiate terms, and complete purchases without human intervention, working across any compatible commerce platform.

Why should businesses implement UCP?

UCP adoption reduces integration costs, opens revenue channels to AI-driven buyers, and future-proofs commerce infrastructure as agentic purchasing becomes mainstream.

Leave a Reply