UCP Payment Processing and Transaction Fees Explained

The Universal Commerce Protocol (UCP) represents a fundamental shift in how payments are processed across distributed commerce ecosystems. Unlike traditional payment gateways that operate within siloed systems, UCP enables seamless payment processing across multiple merchants, platforms, and AI agents. Understanding how UCP handles transactions and manages fees is critical for merchants, developers, and commerce professionals looking to optimize their payment infrastructure.

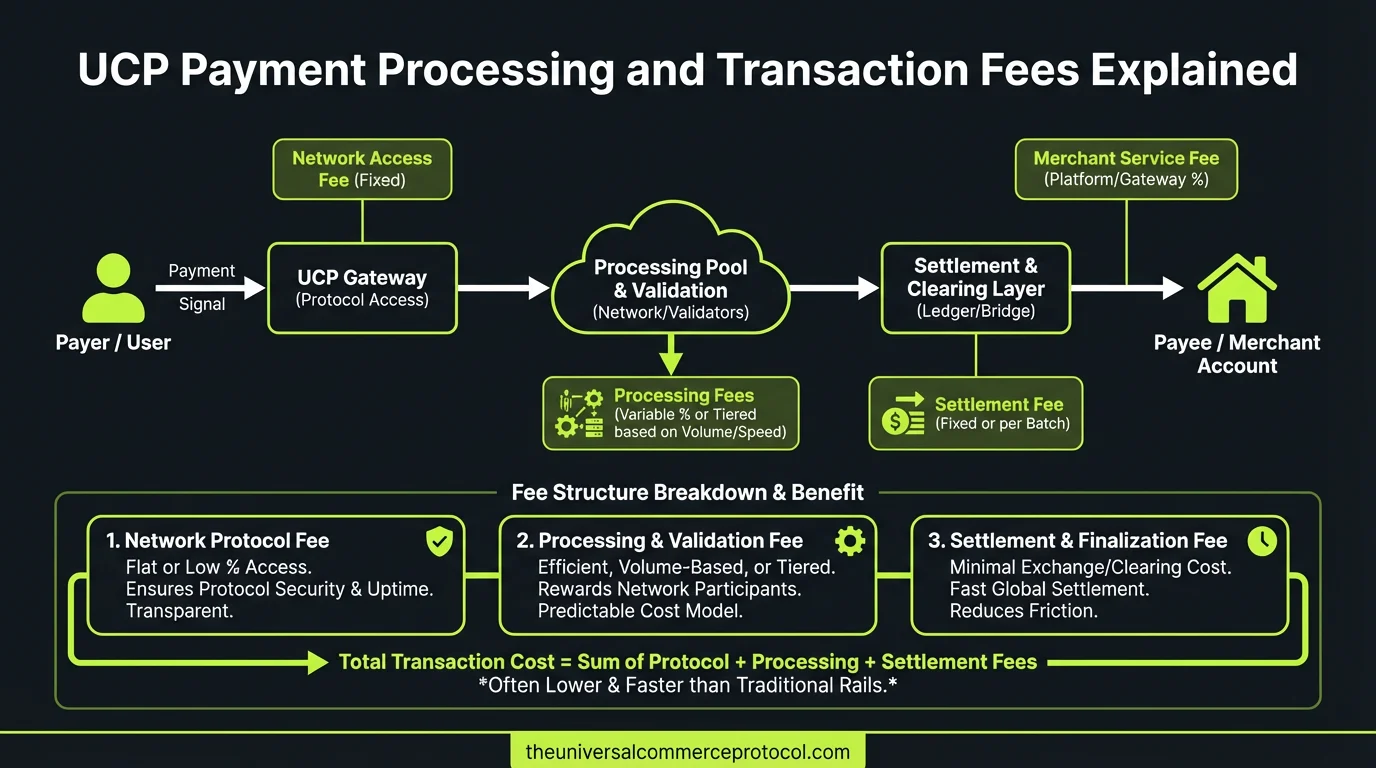

What is UCP Payment Processing?

UCP payment processing is a standardized framework for handling financial transactions across autonomous and traditional commerce systems. It abstracts away the complexity of multiple payment providers, settlement systems, and currency conversions, presenting a unified interface for processing payments regardless of the underlying payment method or merchant location.

Related articles: UCP Shipping Carrier Selection & Rate Optimization • UCP Security Best Practices for AI-Driven Commerce

At its core, UCP payment processing includes:

- Transaction initiation and validation

- Payment method tokenization and storage

- Multi-currency conversion and settlement

- Dispute resolution and chargeback handling

- Real-time transaction reporting and reconciliation

- Compliance with regional payment regulations

The protocol enables AI agents, voice commerce systems, and traditional e-commerce platforms to process payments using identical transaction flows, reducing complexity and improving security across the entire commerce ecosystem.

Understanding UCP Transaction Fee Structures

Interchange Fees

Interchange fees represent the cost paid by acquiring banks to issuing banks for processing card transactions. In UCP systems, these fees are typically transparent and passed through to merchants based on card type, transaction amount, and merchant category code (MCC).

Standard interchange rates typically range from 1.5% to 3.5% depending on:

- Card Type: Credit cards incur higher interchange than debit cards

- Transaction Method: Card-present transactions have lower rates than card-not-present (CNP)

- Merchant Category: High-risk categories (travel, digital goods) pay premium rates

- Transaction Size: Larger transactions may qualify for volume discounts

UCP platforms typically negotiate interchange rates at scale and pass tiered benefits to merchants based on transaction volume and payment method mix.

Processing Fees

Processing fees cover the cost of payment gateway operations, fraud prevention, and transaction routing. In UCP systems, these are usually structured as a percentage of transaction value (typically 0.5% to 1.5%) plus a per-transaction flat fee (usually $0.15 to $0.30).

The formula typically looks like:

Processing Fee = (Transaction Amount × Percentage Rate) + Flat Fee

For example, a $100 transaction with 1% + $0.25 fees would cost: ($100 × 0.01) + $0.25 = $1.25

Settlement and Clearing Fees

Settlement fees cover the cost of moving funds from payment processors to merchant bank accounts. UCP systems typically offer multiple settlement options:

- Standard Settlement (1-2 business days): No additional fee

- Next-Day Settlement: $0.25-$0.50 per batch

- Same-Day Settlement: 0.5%-1% of settlement amount

- Instant Settlement: 1%-2% of settlement amount

Merchants processing high-volume or time-sensitive transactions (like digital goods fulfillment) often utilize faster settlement options to improve cash flow.

Cross-Border and Multi-Currency Fees

UCP’s multi-currency capabilities introduce additional fee considerations:

- Currency Conversion Markup: Typically 2%-3% above interbank rates

- International Interchange: 1%-2% higher than domestic rates

- Regional Payment Method Fees: Local payment methods (iDEAL, Alipay, etc.) may have specific fees

- Cross-Border Settlement Fees: $0.50-$2.00 per transaction

For merchants operating globally, understanding these fees is essential for accurate pricing and margin calculations.

Fee Optimization Strategies for Merchants

Payment Method Routing

UCP enables intelligent payment method routing to minimize fees. Merchants can configure rules that direct transactions to lower-cost payment methods based on customer geography, transaction amount, and historical success rates.

For example:

- Route EU customers to local payment methods (SEPA, Bancontact) with lower fees

- Direct high-value transactions to corporate cards with fixed interchange

- Offer ACH transfers for B2B transactions with reduced fees

- Prioritize digital wallets (Apple Pay, Google Pay) which often have lower interchange

Volume-Based Negotiation

UCP platforms typically offer tiered pricing based on monthly transaction volume. Merchants should:

- Track cumulative monthly volume to identify tier advancement opportunities

- Negotiate rates based on growth projections and commitment periods

- Combine volume across multiple business units if applicable

- Review rates quarterly and request reductions based on performance

Many UCP providers offer volume discounts at thresholds like $10,000, $50,000, $250,000, and $1,000,000 monthly transaction volume.

Pricing Strategy Alignment

Merchants should align their pricing strategy with fee structures:

- Surcharging: Pass payment processing fees directly to customers (where legal)

- Payment Method Incentives: Offer discounts for lower-cost payment methods

- Subscription Models: Reduce per-transaction fees through predictable revenue

- Bulk Purchasing: Offer volume discounts that offset payment processing costs

Developer Considerations for Payment Processing

Fee Calculation and Transparency

When integrating UCP payment processing, developers should implement transparent fee calculations that inform customers before transaction completion. The UCP specification requires:

- Itemized fee breakdown in transaction responses

- Real-time fee estimation based on payment method selection

- Clear communication of settlement timing and associated costs

- Detailed transaction receipts including all fees

Example fee response structure:

{"transaction_id": "txn_123", "amount": 100.00, "currency": "USD", "fees": {"interchange": 1.50, "processing": 0.50, "gateway": 0.25, "total": 2.25}, "net_amount": 97.75, "settlement_date": "2024-01-15"}

Webhook Integration for Fee Events

UCP webhooks provide real-time notifications for fee-related events. Developers should implement handlers for:

payment.fee_calculated– Initial fee estimationpayment.fee_adjusted– Post-authorization fee adjustmentspayment.dispute_fee_applied– Chargeback fee notificationssettlement.fee_deducted– Confirmation of fee deduction from settlement

These webhooks enable real-time reconciliation and accurate financial reporting.

Fee Forecasting and Reporting

UCP platforms provide APIs for fee analysis and forecasting. Developers should implement dashboards that display:

- Historical fee trends by payment method

- Projected monthly fees based on current transaction patterns

- Fee breakdown by transaction type and merchant category

- Comparison of actual vs. estimated fees for accuracy validation

Compliance and Regulatory Fee Considerations

Different jurisdictions impose specific requirements on payment processing fees:

- EU: Capped interchange fees (0.3% for credit cards, 0.05% for debit cards) under PSD2

- US: No interchange caps; Durbin Amendment applies to large banks

- UK: Similar to EU post-Brexit, with FCA oversight

- Asia-Pacific: Varying regulations by country; some regions require local payment processors

UCP payment processors must ensure compliance with these regulations and adjust fee structures accordingly for each market.

Cost Comparison: UCP vs. Traditional Payment Gateways

UCP payment processing typically offers cost advantages over traditional gateways for multi-channel commerce:

| Feature | Traditional Gateway | UCP Platform |

|---|---|---|

| Interchange | 3%-4% | 2%-3% |

| Processing Fee | 1.5%-2.5% | 0.5%-1.5% |

| Multi-Currency | 3%-4% markup | 2%-3% markup |

| Settlement | $0.50-$1.00 | Included/tiered |

| Monthly Minimum | Often $30-$100 | Typically waived |

For merchants processing $100,000 monthly with multi-currency needs, UCP platforms can save $1,500-$3,000 annually compared to traditional gateways.

Future of UCP Payment Fees

As UCP adoption increases, fee structures are likely to evolve:

- AI-Driven Pricing: Dynamic fees based on real-time fraud risk and transaction characteristics

- Blockchain Settlement: Lower fees through direct blockchain-based settlement

- Subscription Models: Flat monthly fees replacing percentage-based pricing

- Competitive Pressure: Downward fee pressure as more platforms adopt UCP

FAQ: UCP Payment Processing and Transaction Fees

Q: What’s included in UCP transaction fees?

A: UCP transaction fees typically include interchange (paid to issuing banks), processing fees (gateway operations and fraud prevention), and settlement fees (moving funds to merchant accounts). Some UCP platforms bundle these into a single percentage rate, while others itemize them separately. Always request a detailed fee breakdown from your UCP provider.

Q: Can merchants reduce UCP payment processing fees?

A: Yes, through several strategies: increasing transaction volume to access tier discounts, optimizing payment method routing to lower-cost options, negotiating rates based on business projections, and aligning pricing strategy to offset costs. Merchants processing $50,000+ monthly should actively negotiate with providers.

Q: How do multi-currency transactions affect UCP fees?

A: Multi-currency transactions typically incur 2-3% currency conversion markup above interbank rates, plus higher international interchange fees (1-2% above domestic rates). Some UCP platforms offer better rates for high-volume multi-currency merchants through negotiated agreements.

Q: What’s the difference between UCP and traditional payment gateway fees?

A: UCP platforms typically offer lower fees (0.5-1.5% processing vs. 1.5-2.5% for traditional gateways) due to scale and unified processing. UCP also eliminates separate fees for multi-channel integration and provides better multi-currency rates. However, fee comparison should be based on your specific transaction profile.

Q: Are UCP payment fees compliant with regional regulations?

A: Reputable UCP platforms ensure compliance with regional fee caps (like EU’s PSD2 interchange limits) and adjust pricing accordingly by geography. Verify your provider’s compliance certifications and request documentation of fee structures for your specific operating regions.

What is UCP Payment Processing?

UCP (Universal Commerce Protocol) payment processing is a standardized framework for handling financial transactions across autonomous and traditional commerce systems. It abstracts the complexity of multiple payment providers, settlement systems, and currency conversions into a unified interface that works regardless of the underlying payment method or merchant location.

How does UCP differ from traditional payment gateways?

Unlike traditional payment gateways that operate within siloed systems, UCP enables seamless payment processing across multiple merchants, platforms, and AI agents. This distributed approach provides greater flexibility and integration capabilities compared to conventional payment processing infrastructure.

What core functions does UCP payment processing include?

UCP payment processing includes transaction initiation and validation, payment method tokenization and storage, multi-currency conversion and settlement, and dispute resolution and chargeback handling. These functions work together to provide comprehensive payment management across distributed commerce ecosystems.

Who should use UCP payment processing?

UCP payment processing is ideal for merchants, developers, and commerce professionals looking to optimize their payment infrastructure across multiple platforms and merchants. It’s particularly valuable for those operating in distributed commerce ecosystems or working with AI agents and autonomous systems.

What is the key benefit of UCP’s unified approach to payments?

The key benefit of UCP’s unified interface is that it simplifies payment processing by handling multiple payment providers, settlement systems, and currency conversions transparently. This allows merchants to process payments seamlessly across different platforms and locations without managing complexity of individual payment systems.

Frequently Asked Questions

What is the Universal Commerce Protocol (UCP)?

The Universal Commerce Protocol (UCP) is an open standard developed to enable AI agents to autonomously conduct commerce transactions across any platform.

How does UCP enable agentic commerce?

UCP provides standardized APIs and protocols so AI agents can discover products, negotiate terms, and complete purchases without human intervention, working across any compatible commerce platform.

Why should businesses implement UCP?

UCP adoption reduces integration costs, opens revenue channels to AI-driven buyers, and future-proofs commerce infrastructure as agentic purchasing becomes mainstream.

Leave a Reply