What Are Agentic Payments?

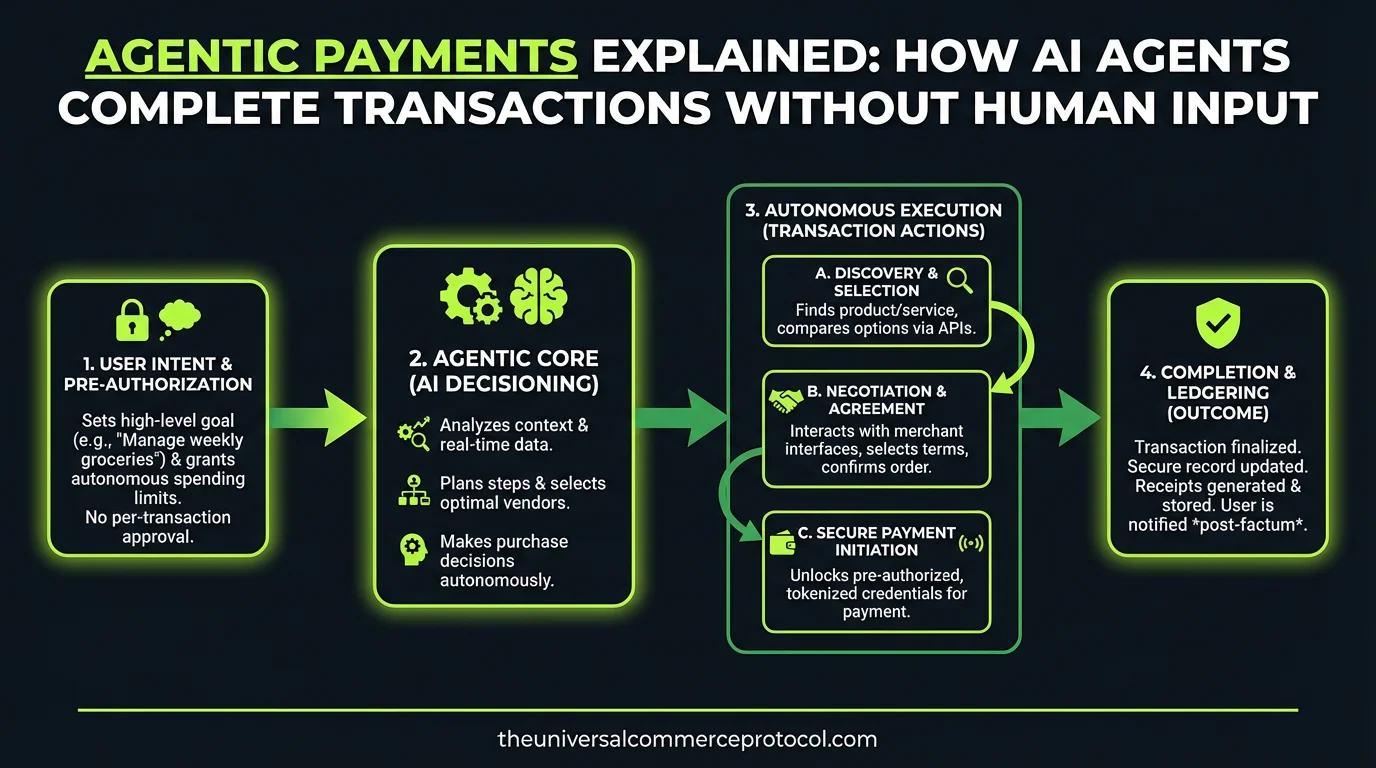

Agentic payments are financial transactions initiated, authorized, and completed by artificial intelligence agents without direct human intervention at the point of sale. Unlike traditional e-commerce where a human user clicks “buy” or enters payment details, agentic payments allow autonomous systems to assess conditions, evaluate options, and execute payments based on predetermined rules, real-time data, and machine learning models.

This represents a fundamental evolution in payment infrastructure. Rather than payments being reactive (triggered by human action), they become proactive and contextual—an AI agent monitoring your inventory might automatically purchase replacement stock when levels fall below threshold, or an autonomous vehicle might pay for charging services as it approaches a charging station.

The distinction between agentic payments and traditional APIs lies in autonomy and decision-making. Standard payment APIs require explicit human authorization for each transaction. Agentic payments operate within delegated authority frameworks where the human has pre-authorized the agent to make decisions within specific parameters—spending limits, merchant categories, time windows, or outcome-based conditions.

The Architecture of Autonomous Payment Flows

Core Components

Agentic payment systems require several interconnected layers to function securely and reliably:

- Agent Layer: The AI system that perceives conditions, makes decisions, and initiates transactions. This might be a large language model (LLM), a specialized machine learning model, or a rules-based system.

- Authorization Framework: The governance layer that defines what an agent can and cannot do—spending caps, merchant whitelists, transaction frequency limits, and approval thresholds.

- Payment Protocol: The standardized interface through which agents communicate payment intent. The Universal Commerce Protocol (UCP) serves this function for agentic commerce.

- Settlement Infrastructure: The underlying payment networks (ACH, card networks, blockchain networks) that actually move funds.

- Audit and Compliance Layer: Real-time monitoring, logging, and reporting systems that ensure transactions comply with regulatory requirements and organizational policies.

Decision Flow in Agentic Payments

A typical agentic payment flow follows this sequence:

- Perception: The agent monitors relevant data streams—inventory levels, market prices, weather forecasts, customer demand signals, or supply chain status.

- Analysis: The agent evaluates current conditions against its decision models and the parameters defined by its human operators.

- Intent Formation: If conditions warrant action, the agent formulates a specific payment intent—”purchase 500 units of component X from supplier Y at price Z.”

- Authorization Check: The agent verifies that the proposed transaction falls within its delegated authority—budget remaining, merchant approval, transaction size limits.

- Protocol Submission: The agent submits the transaction through UCP or similar standards, providing structured data about what it wants to buy, from whom, and under what terms.

- Execution: The payment network processes the transaction, routing it through appropriate settlement systems.

- Confirmation and Learning: The agent receives confirmation, logs the transaction, and may update its models based on outcomes.

The Universal Commerce Protocol’s Role

Standardizing Agentic Commerce

The Universal Commerce Protocol provides the semantic and technical standard that allows AI agents to express payment intent in a way that payment processors, merchants, and financial institutions can reliably interpret and act upon.

Without standardization, each agent-payment system integration would require custom development. UCP solves this by providing:

- Structured Intent Expression: A standardized way for agents to describe what they want to purchase, from whom, at what price, and under what conditions.

- Trust Negotiation: Mechanisms for agents and merchants to establish mutual trust without requiring pre-existing relationships or human intermediation.

- Capability Advertisement: Protocols for merchants to communicate what they can sell, what payment methods they accept, and what terms they offer.

- Atomic Transactions: Guarantees that payment and delivery are tightly coupled—either both occur or neither does.

- Audit Trail: Built-in logging that creates immutable records of agent decisions and actions for compliance and transparency.

UCP and Delegation Chains

A critical UCP capability for agentic payments is support for delegation chains—scenarios where authority flows through multiple layers. For example:

A CFO authorizes an AI procurement agent with a $1 million quarterly budget. That agent can further delegate authority to sub-agents managing specific categories (logistics, raw materials, services). Each sub-agent operates within its delegated scope, but all transactions flow through the same UCP-compliant audit trail, allowing the CFO to maintain visibility and control.

This hierarchical delegation is impossible with traditional payment APIs but essential for agentic commerce at scale.

Real-World Agentic Payment Scenarios

Supply Chain Automation

Consider a manufacturing company using an AI-powered supply chain orchestration system. As production lines consume raw materials, IoT sensors feed real-time inventory data to the agent. When inventory of a critical component falls below the reorder point, the agent:

- Queries multiple suppliers via UCP for current pricing and availability

- Evaluates options based on cost, delivery time, and supplier reliability scores

- Selects the optimal supplier and automatically initiates a purchase order

- Triggers payment upon confirmed shipment

Companies like Coupa and Jaggr are moving toward this model, though most still require human approval checkpoints. True agentic payments would eliminate those checkpoints within defined parameters.

Autonomous Vehicle Charging and Services

An autonomous vehicle (AV) fleet operated by a company like Waymo or Cruise needs to autonomously pay for charging, parking, tolls, and maintenance. The fleet management agent:

- Continuously monitors vehicle battery levels, location, and service needs

- Identifies optimal charging stations or service providers using real-time pricing data

- Initiates payments directly with charging infrastructure providers or service vendors

- Executes transactions through UCP-compliant payment flows

This eliminates the need for human fleet managers to manually authorize each transaction while maintaining detailed audit trails for cost allocation and tax compliance.

Dynamic Pricing and Hedging

Financial trading firms use AI agents to execute trades based on market conditions. While trading has long used automated execution, agentic payments extend this to include automatic settlement and hedging payments. An agent might:

- Detect market opportunities through real-time data analysis

- Execute trades automatically

- Initiate collateral payments to clearinghouses

- Execute hedging transactions to manage risk exposure

Firms like Citadel and Two Sigma already use sophisticated algorithmic trading, but UCP standardization would enable more seamless multi-party settlement.

Security and Trust in Agentic Payments

Authorization and Limits

The foundation of secure agentic payments is granular authorization. Humans define what agents can do through policies that specify:

- Total spending caps (daily, weekly, monthly, quarterly)

- Per-transaction limits

- Approved merchant categories or specific merchants

- Allowed payment methods

- Geographic or temporal restrictions

- Approval thresholds (transactions above $X require additional authorization)

Anomaly Detection and Circuit Breakers

Agentic payment systems must include real-time monitoring that detects unusual patterns. If an agent suddenly begins making transactions outside its normal behavior profile, the system should:

- Flag the transaction for human review

- Temporarily suspend the agent’s authority

- Alert compliance and security teams

- Provide detailed context about what triggered the alert

Cryptographic Verification

UCP incorporates cryptographic signing to ensure that transactions genuinely originate from authorized agents and haven’t been tampered with. Each transaction includes:

- Digital signatures proving the agent’s identity

- Timestamps proving when the transaction was initiated

- Merkle proofs linking the transaction to the agent’s authorization framework

Regulatory and Compliance Considerations

Consumer Protection

Agentic payments in consumer contexts (e.g., an AI assistant making purchases on your behalf) must comply with regulations like the Electronic Funds Transfer Act (EFTA) and similar frameworks globally. Key requirements include:

- Clear disclosure of what the agent is authorized to do

- Easy mechanisms to revoke agent authority

- Liability protection if the agent is compromised

- Regular statements showing agent-initiated transactions

Commercial and B2B Compliance

Business-to-business agentic payments face different regulatory landscapes depending on jurisdiction and industry. Financial services firms face particularly stringent requirements around:

- Know Your Customer (KYC) verification

- Anti-Money Laundering (AML) compliance

- Transaction monitoring and reporting

- Audit trail maintenance

UCP’s built-in audit capabilities help organizations meet these requirements by creating immutable, timestamped records of every agent-initiated transaction.

The Future of Agentic Payments

As AI capabilities mature and UCP adoption increases, agentic payments will become increasingly sophisticated. We can expect:

- Cross-border agentic payments: Agents negotiating and executing transactions across currency and regulatory boundaries

- AI-to-AI commerce: Agents from different organizations directly transacting without human intermediation

- Predictive procurement: Agents anticipating future needs and pre-positioning inventory or capacity

- Micro-transaction proliferation: Agentic payments enabling economically viable transactions too small for traditional payment processing

- Conditional payments: Payments that execute only when specific conditions are met, verified through smart contracts or oracles

FAQ

What’s the difference between agentic payments and automated payments?

Automated payments follow rigid, pre-programmed rules (e.g., “pay this invoice on the 15th of each month”). Agentic payments involve AI systems that perceive changing conditions, make contextual decisions, and adapt their behavior based on real-time data and learned patterns. An agent can decide to buy from a different supplier if prices change or quality scores shift.

Are agentic payments already in use?

Partially. Algorithmic trading systems execute automated payments and settlements at scale. Supply chain software increasingly automates purchase orders. However, these systems typically operate within proprietary frameworks, not standardized protocols like UCP. True agentic payments—using standardized protocols, operating across organizational boundaries, and making contextual decisions—are still emerging.

What happens if an AI agent makes a payment mistake?

This depends on the authorization framework and transaction terms. If an agent operates within its defined authority and the transaction is valid, the payment stands—the agent’s operators bear the cost. However, if the agent exceeds its authority or the transaction violates its parameters, the payment can be reversed. UCP’s audit trail makes it easy to investigate and prove what happened.

How does UCP ensure agents don’t get hacked and make unauthorized payments?

UCP combines multiple security layers: cryptographic verification that transactions genuinely come from the agent, real-time anomaly detection that flags unusual behavior, spending caps that limit damage even if an agent is compromised, and granular authorization policies that restrict what the agent can do. No single point of failure can enable unlimited unauthorized payments.

Frequently Asked Questions

What are agentic payments?

Agentic payments are transactions initiated and completed by an AI agent on behalf of a human principal, without requiring the human to manually approve each purchase. The agent operates within spending limits and product preferences set in advance, using cryptographic trust frameworks to authenticate with payment networks.

How do AI agents pay for purchases securely?

AI agents use tokenized payment credentials and verifiable intent signals to authenticate with merchants and payment processors. The Universal Commerce Protocol (UCP) provides a standardized layer that lets merchants verify the agent’s identity, spending authority, and transaction integrity before accepting payment.

Are agentic payments safe for merchants?

Yes, when implemented with proper trust frameworks. UCP provides agent authentication, verifiable spending intent, and cryptographic transaction signing that gives merchants stronger fraud signals than traditional card-present or card-not-present transactions. Liability frameworks from Visa and Mastercard are also evolving to cover agent-initiated transactions.

Leave a Reply